2026 Starts With a Big Rotational Change

Recent weeks have brought about a clear shift in market leadership. Technology and financial stocks have lost their edge, giving way to sectors that historically perform well in the later stages of the business cycle. If you're expecting this to be a brief reversal that quickly fades, you may want to consider that over seven decades of business cycle analysis suggest otherwise.

I believe the business cycle should be viewed as a predictable series of events that unfold in a consistent order. A typical cycle begins during a recession or period of slowing growth, marked by an influx of liquidity and declining interest rates. Lower rates breathe life into the interest-sensitive housing market, which, in turn, drives demand for goods like furniture, stimulating manufacturing. As production ramps up, factories eventually hit capacity limits, leading to businesses investing more heavily in capital equipment.

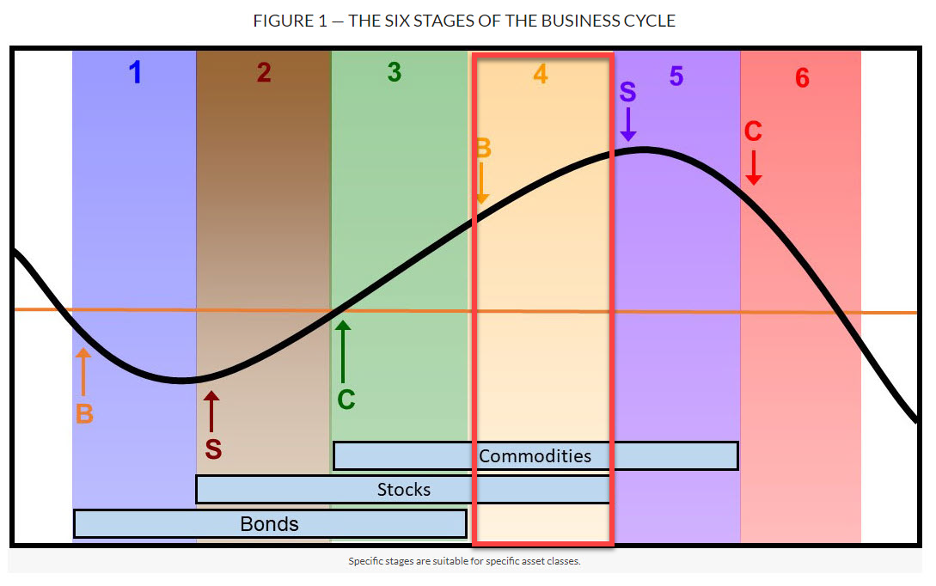

This is, of course, an oversimplification. In reality, hundreds of economic developments are at play. This sequential rotation also influences the major turning points for bonds, stocks, and commodities, each of which has a peak and trough, producing six key inflection points in total, as illustrated in Figure 1 and described in greater detail here.

At Pring Turner, and in the monthly Intermarket Review, we use these six turning points to define distinct stages of the cycle, much like the seasons of the year, each with its own investment implications. Our models currently place the cycle in Stage 4, an environment that is favorable for stocks and commodities while unfavorable for bonds and, notably, the most bullish stage of the cycle for commodity prices.

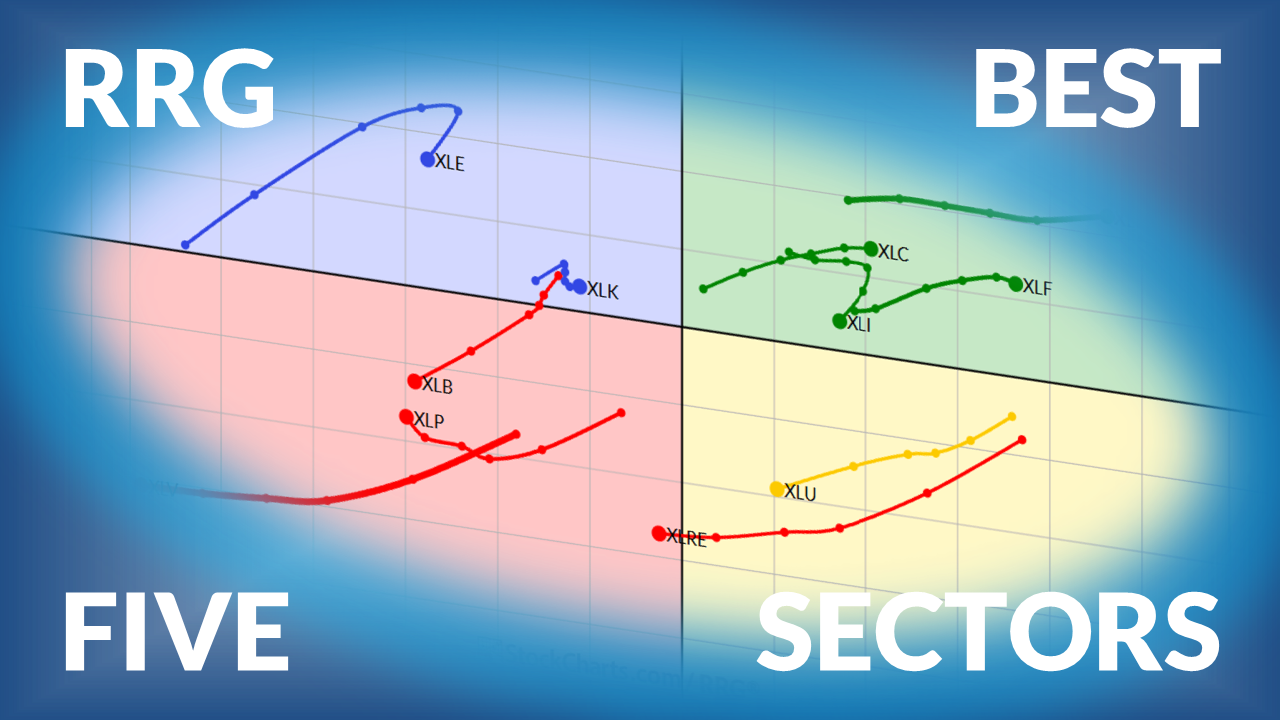

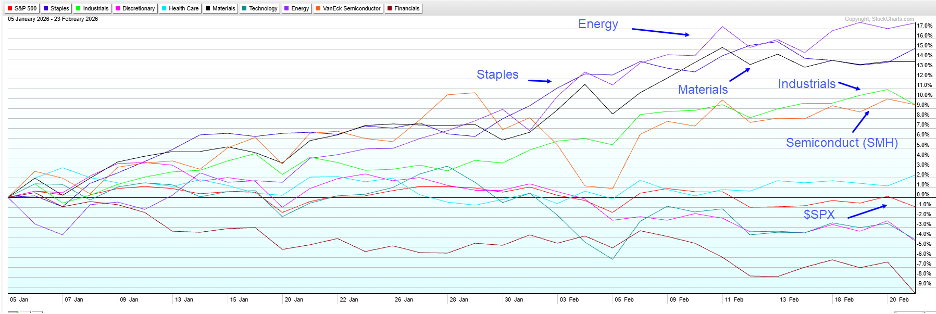

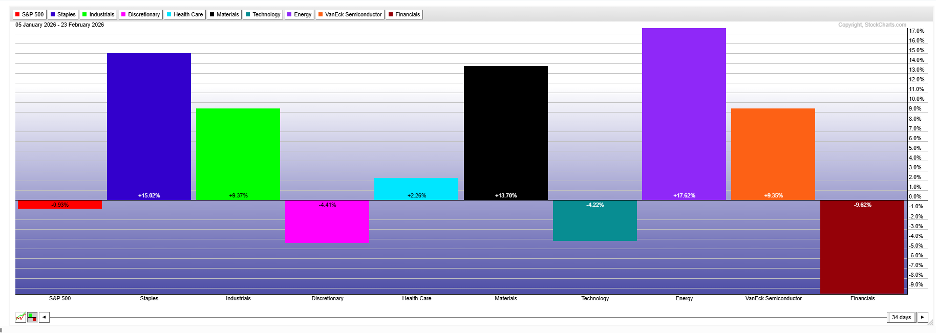

Figure 2 reflects this dynamic, showing selected sector performance since the start of the year. The top-performing sectors are largely those driven by earnings. The notable outlier is Consumer Staples, which is a more defensive play by nature.

As shown in Figure 3, Consumer Discretionary, Technology, and Financials have been the weakest performers year-to-date.

This Rotation is Likely to Last

The next three charts display price action alongside long-term momentum in the upper panels, with relative strength and relative momentum shown below.

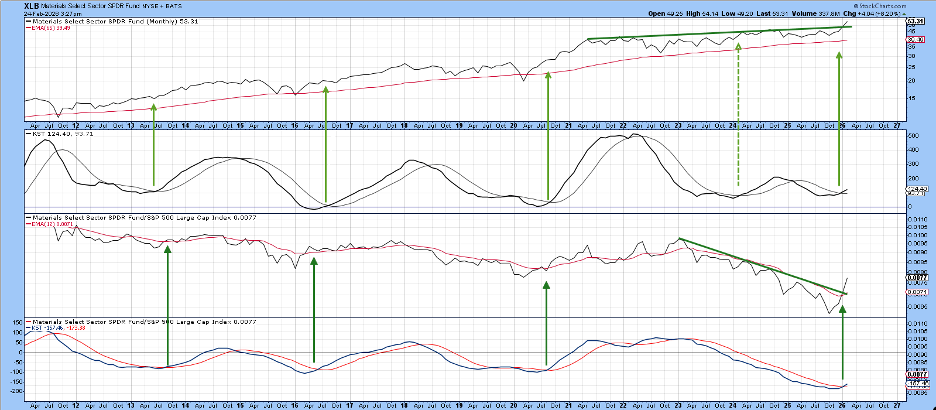

For the Materials Select Sector SPDR ETF (XLB) in Chart 1, price has broken out of a five-year consolidation range, supported by a positive long-term KST reading. On a relative basis, a three-year downtrend line has been broken, accompanied by a long-term KST buy signal. Historical patterns suggest that momentum buy signals of this kind typically precede a two-to-three-year trend change, both in absolute and relative terms.

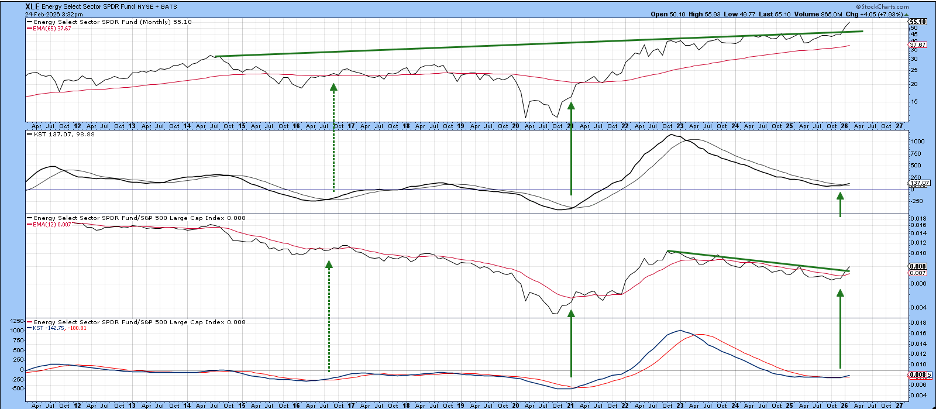

Chart 2 examines the Energy Select Sector SPDR ETF (XLE) in a similar light. The setup mirrors that of XLB, though the resistance trend line here stretches back considerably further, making the breakout even more significant. The 2016 buy signals, shown as dashed lines, ultimately disappointed. However, in 2026, all four indicators have broken through key trend lines and their moving averages, a strong signal that Energy is poised to remain a market leader for the foreseeable future.

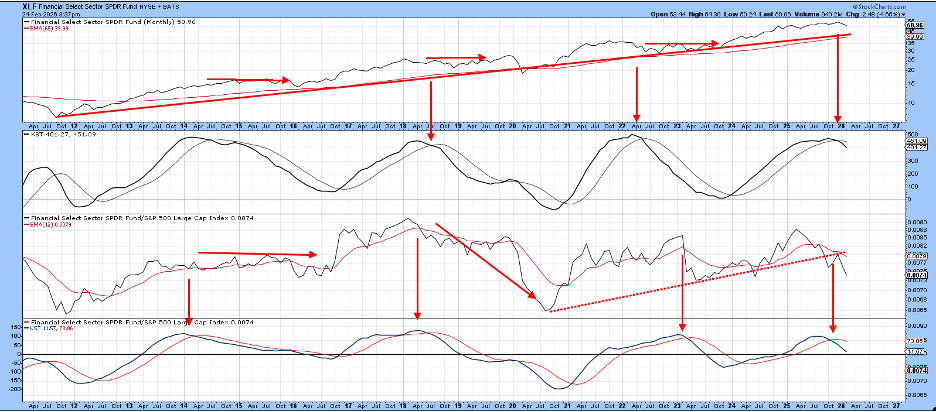

Chart 3 turns to the Financial Select Sector SPDR ETF (XLF) as an example of a sector losing relative ground. It's worth noting that underperformance doesn't necessarily mean price declines. A sector can still rise in price while lagging the broader market. The XLF remains above its long-term uptrend line and 65-month EMA, so the absolute trend is still intact, even as the long-term KST has recently flashed a momentum sell signal. More telling is the relative picture: the RS KST has turned negative, and the relative strength line has broken a five-year uptrend, pointing to continued underperformance ahead regardless of where the price itself goes.

The Bottom Line

The business cycle has entered a phase that rewards sectors tied to capacity constraints and rising commodity prices. Early 2026 sector performance confirms this shift, and the long-term technical picture for Materials and Energy reinforces the view that this change in leadership is not likely to be a fleeting one.

Martin J. Pring

The views expressed in this article are those of the author and do not necessarily reflect the position or opinion of Pring Turner Capital Group of Walnut Creek or its affiliates.