JPMorgan Crumbles as AI Disruption Hit Wall Street's Fortress

Key Takeaways

- JPM's stock price has broken below a key support level with weakening relative strength and momentum.

- A bear put spread options strategy offers a compelling risk/reward structure.

- In this trade setup, you're risking $760 to potentially make $1,740; a 2.3:1 reward-to-risk ratio.

JPMorgan Chase (JPM) just broke below the most closely watched support level in the entire financial sector, and the implications are significant.

After surging to all-time highs near $337 in late January, JPM has been in a downtrend, losing over 12% in less than a month. Today's breakdown below $300, a level that had served as a concrete floor since October 2025, marks a critical technical failure. The stock closed at $297.67, down 4.2% on heavy volume, as the $300 support that held for nearly five months gave way. More concerning is that JPM's relative strength versus the S&P 500 and momentum have turned negative at the same time. JPM stock is now trading below both its 50-day and 20-day moving averages with no visible support until the mid-$270s.

But this isn't just a chart story. The fundamental backdrop is shifting in ways that even the bulls are struggling to dismiss.

The AI Disruption Nobody Saw Coming

Monday's selloff was sparked by a research report from Citrini Research that connected the dots between AI agent adoption and potential credit deterioration across the U.S. financial system. The thesis is straightforward but powerful: as AI agents become ubiquitous, currently used by 40% of Americans at least once a week and growing rapidly, they will automate everything from shopping to subscription cancellation, compressing margins across industries. Citrini's bear case projects that, by 2028, AI agents could drive unemployment to 10% and put half of all white-collar workers out of their jobs.

For JPMorgan, the transmission mechanism is direct. White-collar professionals account for approximately 75% of U.S. discretionary consumer spending and represent the bank's highest-quality borrower cohort. A meaningful disruption to this demographic doesn't just reduce loan demand, it threatens credit quality across JPM's $1.3 trillion consumer lending portfolio, particularly the revolving credit card balances that have been a key revenue growth driver.

The Expense Bomb and Slowing Momentum

The AI headline landed on top of cracks that were already forming. When JPMorgan reported Q4 2025 earnings, the headline numbers looked solid - adjusted EPS of $5.23 beat consensus by 7.6%, and equities trading revenue surged 40%. But beneath the surface, the market found reasons to worry.

The 2026 expense guidance was the real shock. Management projected expenses ballooning to $105 billion, up from $96 billion in 2025, an increase that sent the stock sliding 3.8% on earnings day alone. Analyst Mike Mayo pressed CEO Jamie Dimon on the call for more granularity, particularly around the bank's surging tech and AI spend. Dimon's response was essentially "trust us”, telling analysts they'd "be justified by the results" without providing breakdowns. That kind of opacity doesn't inspire confidence when you're asking shareholders to absorb a 9.4% expense increase.

Add to that a $2.2 billion credit reserve for the Apple Card portfolio acquisition from Goldman Sachs, which hit Q4 earnings by $0.60/share and eroded the Advanced CET1 capital ratio by 90 basis points. Investment banking fees also unexpectedly declined in Q4, missing the firm's own guidance from just a month prior.

The Regulatory Overhang

The "risk cocktail" doesn't stop there. The proposed 10% cap on credit card interest rates remains a live regulatory threat. If enacted, it would compress margins across JPM's consumer credit division. The bank just doubled down in this segment with the Apple Card acquisition.

Meanwhile, mounting concerns about private credit valuations, amplified by recent headlines around Blue Owl halting redemptions, are making people nervous about the "private credit" market. Since JPMorgan provides financing and risk management to alternative lenders, it could feel the tremors first.

The Bull Case Is Fading

To be fair, JPMorgan remains a fortress. Full-year 2025 delivered $57 billion in net income, a 20% ROTCE, and the bank's asset and wealth management division hit record revenue of $6.5 billion. The consensus analyst rating is still "Buy" with an average price target around $333. But consensus targets are backward-looking; they haven't fully absorbed today's breakdown, the AI disruption narrative, or the compounding headwinds from expense inflation and regulatory risk.

When the best-in-class bank in America breaks its most important support level on heavy volume with deteriorating relative strength, the message is clear: institutional money is rotating out, and the path of least resistance is lower.

A Bearish Strategy Worth Your Attention

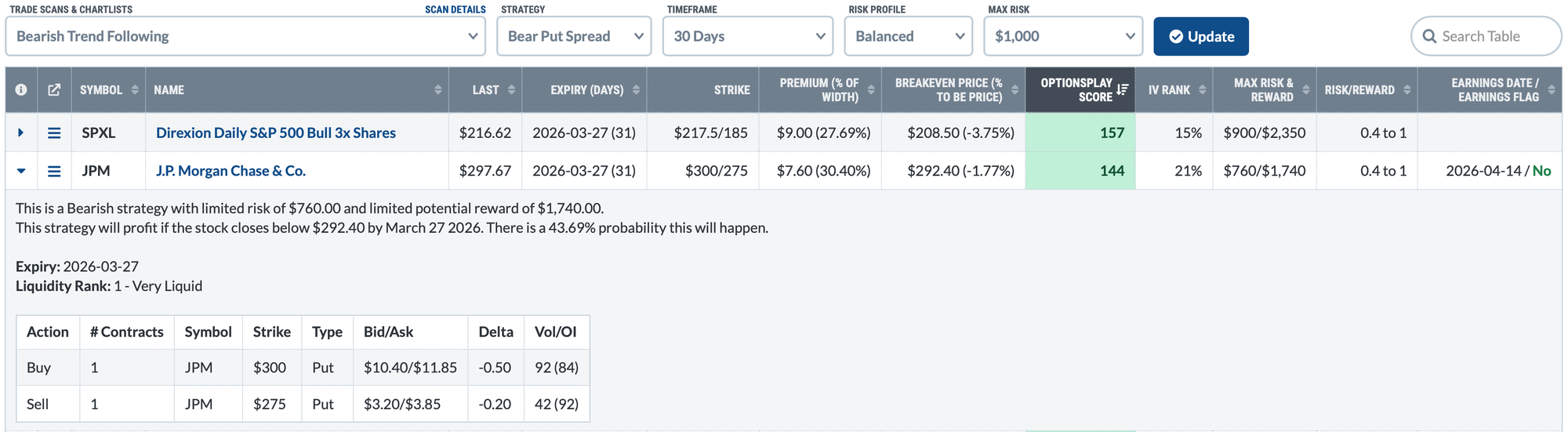

This is where the opportunity gets interesting. OptionsPlay's Bearish Trend Following scan, designed to surface stocks showing sustained technical weakness, flagged JPM with an OptionsPlay Score of 144 and highlighted a Bear Put Spread as one of the most compelling risk/reward structures available.

Here's the setup:

Buy to Open the March 27, 2026 $300/275 Put Spread @ $7.60 Debit

Net Debit: ~$7.60 (30.4% of the $25 spread width)

Max Risk: $760

Max Reward: $1,740

Breakeven: $292.40 (-1.77% from current price)

Probability of Profit: 43.69%

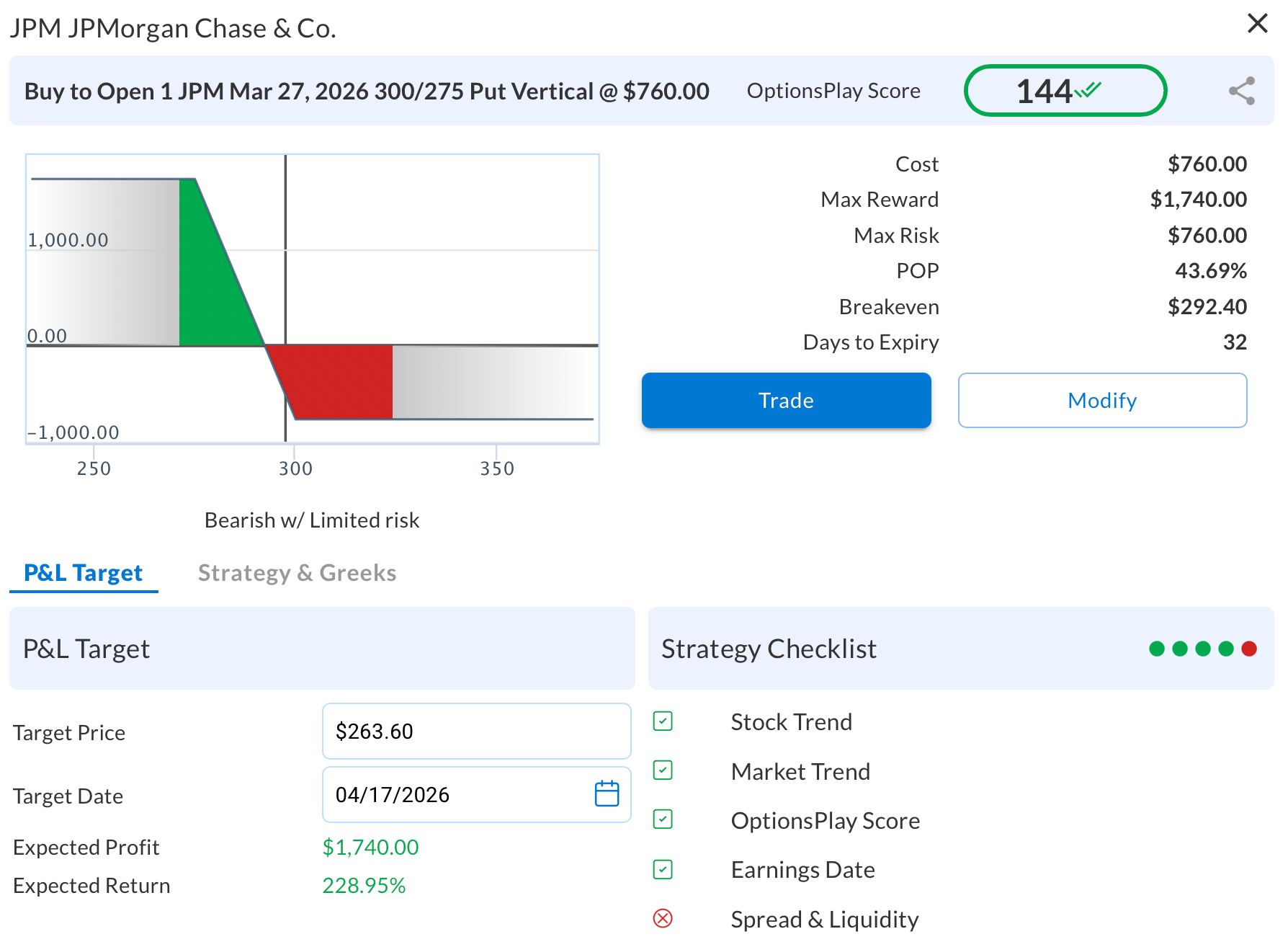

Why is this structure so attractive? Because the premium you're paying — 30.4% of the spread width — means you're risking $760 to potentially make $1,740, a 2.3:1 reward-to-risk ratio. And your breakeven at $292.40 is only 1.77% below the current price, meaning the stock barely needs to move further for the trade to start working. With 31 days until expiration and JPM's IV rank at 21% (still relatively elevated), the put spread captures bearish directional exposure without the full cost of an outright put purchase.

The timing is noteworthy. JPM's next earnings report isn't until April 14, so the March 27 expiration avoids earnings event risk entirely. You're betting purely on the continuation of the technical breakdown and the market's repricing of the AI disruption narrative, without the binary wildcard of an earnings announcement.

Finding the Setup in Seconds

Identifying a stock that has both the perfect technical breakdown and an optimally priced options strategy is time-consuming. You'd need to screen for bearish momentum, check relative strength, analyze the options chain for favorable skew, and calculate breakevens and reward-to-risk. That's easily 15–20 mins of work per idea with countless unviable trades along the way.

Or you could do what we did: run the Bearish Trend Following scan inside OptionsPlay's Strategy Center, filter for Bear Put Spreads within 30 days, set a balanced risk profile with $1,000 max risk, and find JPM sitting right near the top of the list, in under 5 seconds.

This is how OptionsPlay can help you identify actionable trades just like this within seconds. The OptionsPlay integration does the heavy lifting, combining technical scanning with real-time options analytics so you can move from idea to execution in the time it takes most traders to open a single options chain. The tool ignored the emotional panic and focused on the math: JPM is at risk of tumbling and the options markets are misplacing that risk.

See the opportunities you’re missing. Unlock the full potential of your ChartLists with the OptionsPlay Add-On.