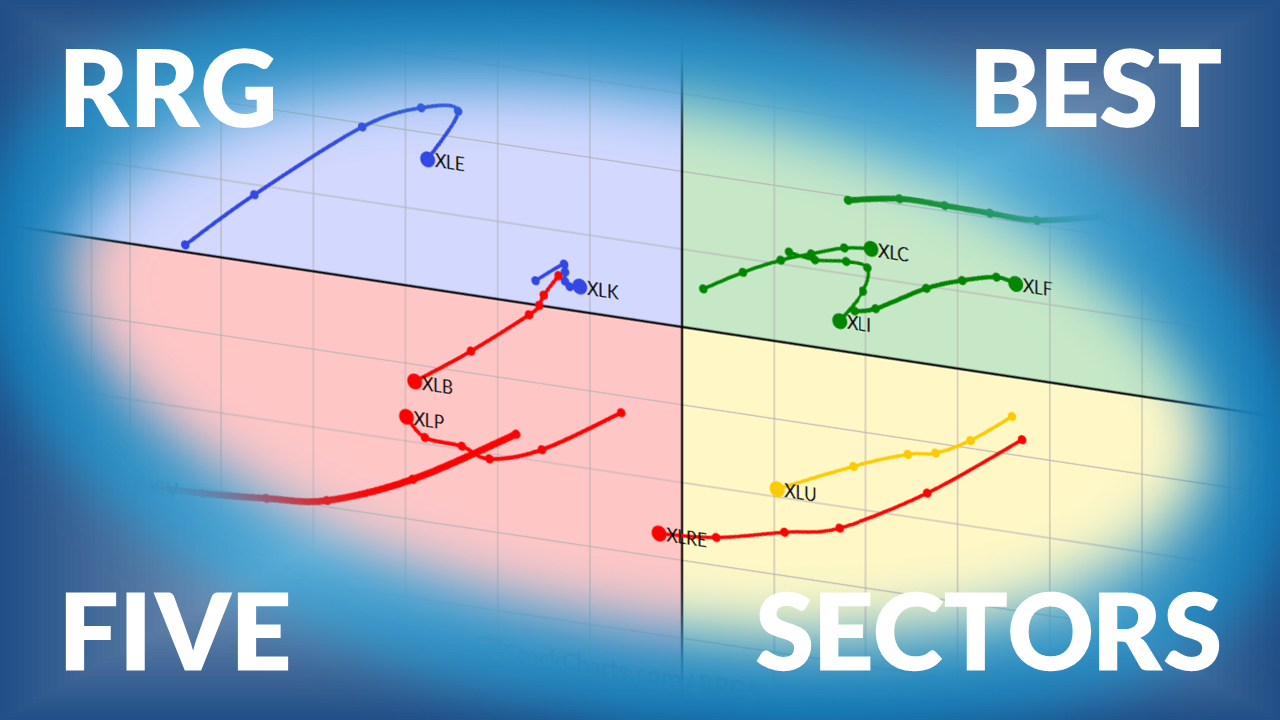

The Best Five Sectors This Week #58

Key Takeaways

- Energy, Materials, Industrials, Utilities, and Staples maintain their lead.

- Energy remains the top-performing sector, showing strong momentum on both weekly and daily RRG charts.

- Technology, Consumer Discretionary, and Financials continue to underperform deep inside the lagging quadrant.

- Sustained rotation into defensive sectors indicates that investors remain wary of ongoing market volatility.

Defensive Sectors Hold Steady Amid Market Volatility

After a week in which the S&P 500 dropped roughly 2%, the sector rankings, based on the Relative Rotation Graph (RRG) methodology, remain unchanged.

Despite ongoing market volatility and an unexpected uptick on Monday, the persistence of the top five sectors, especially the defensive ones like Energy, Utilities, and Staples, signals caution. The unchanged rankings suggest that investors are favoring sectors that traditionally offer stability during uncertain times.

- (1) Energy - XLE [15%]

- (2) Materials - XLB [10%]

- (3) Industrials - XLI [40%]

- (4) Utilities - XLU [10%]

- (5) Consumer Staples - XLP [25%]

- (6) Health Care - XLV

- (7) Real Estate - XLRE

- (8) Communication Services - XLC

- (9) Technology - XLK

- (10) Consumer Discretionary - XLY

- (11) Financials - XLF

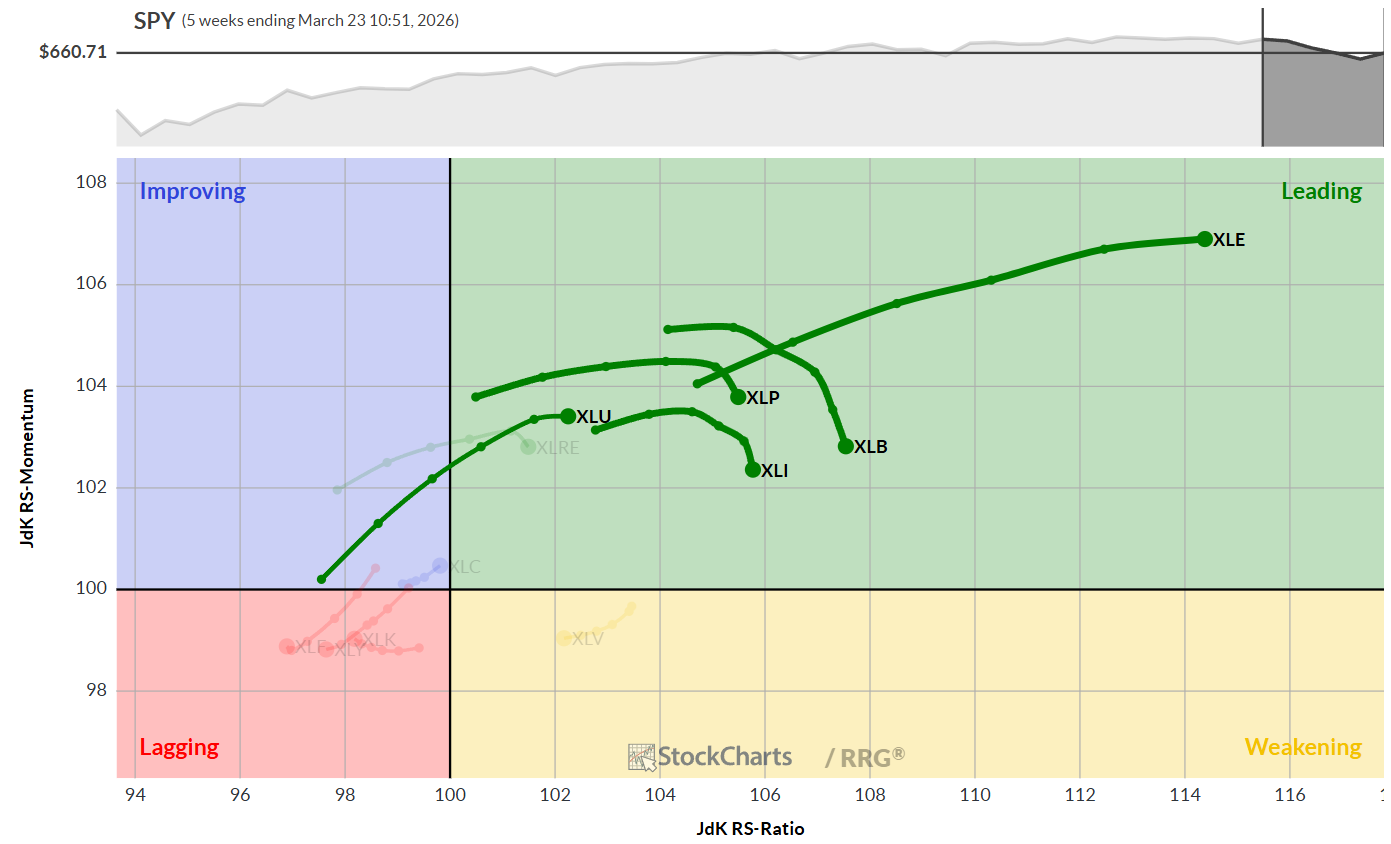

Weekly RRG

On the weekly RRG, all top five sectors remain in the leading quadrant. Energy stands out as the outlier, maintaining a strong positive heading. Utilities also show a positive heading, though with the lowest RS ratio among the top five.

Industrials, Consumer Staples, and Materials are still in the leading quadrant but have started to lose relative momentum, though only mildly and still above the 100 mark.

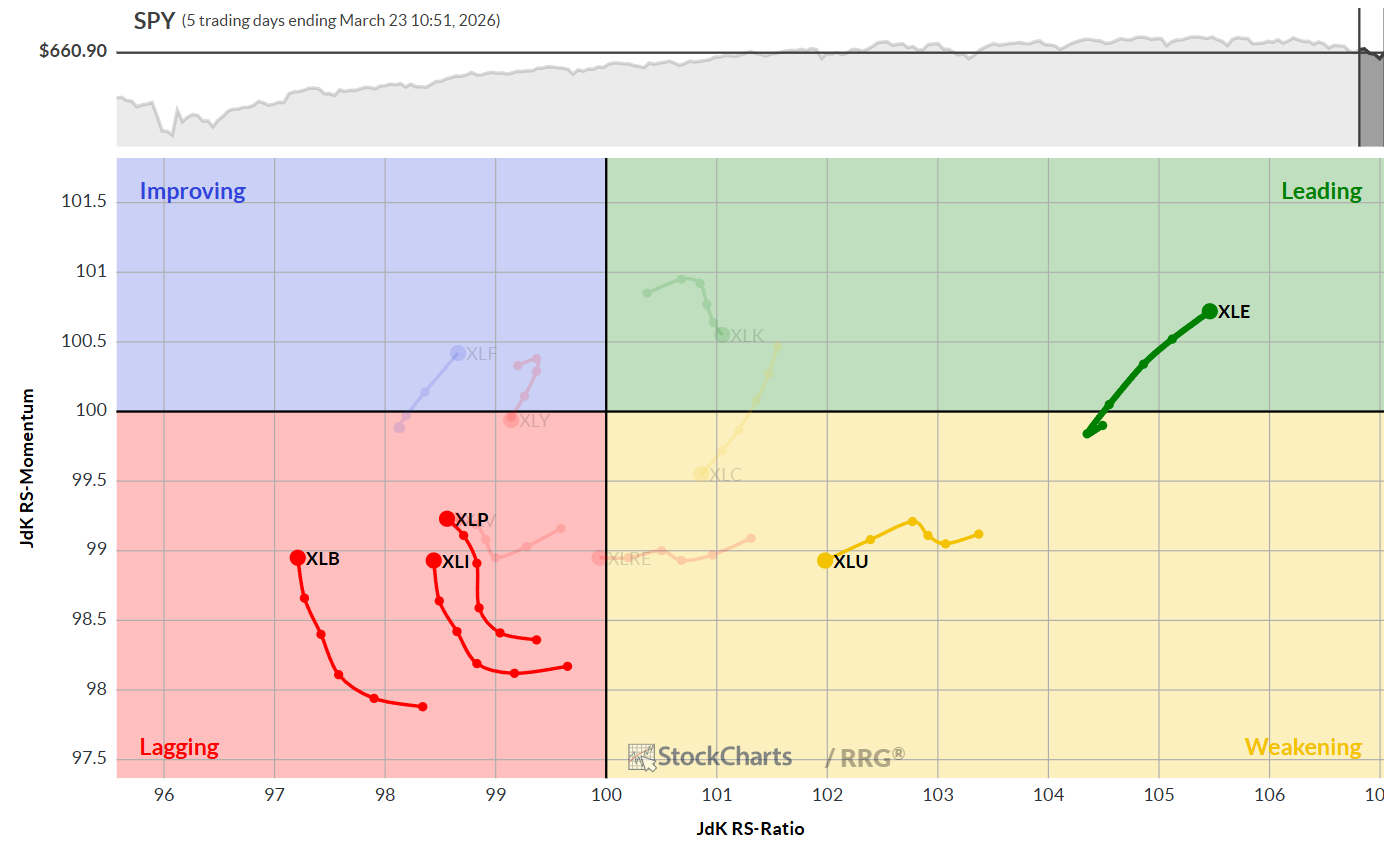

Daily RRG

Energy is the strongest sector, confirming its weekly performance with a rotation back into the leading quadrant on the daily RRG. Utilities remain on the right-hand side, indicating a positive RS ratio, but are experiencing negative momentum and heading. However, Utilities has enough room to rotate back upwards to the leading quadrant.

Materials, Industrials, and Consumer Staples are in the lagging quadrant, but are beginning to pick up relative momentum. Once they achieve a positive heading, their daily RRG tails will likely turn positive, which could also impact their weekly performance.

Defensive positioning continues to dominate, reflecting the market’s cautious sentiment.

A quick look at Technology, Consumer Discretionary, and Financials, sectors with significant market capitalization, shows that their weekly RRG tails are deep in the lagging quadrant and moving further in that direction. These sectors continue to display weak relative strength and momentum, underscoring their underperformance.

Sector Breakdown

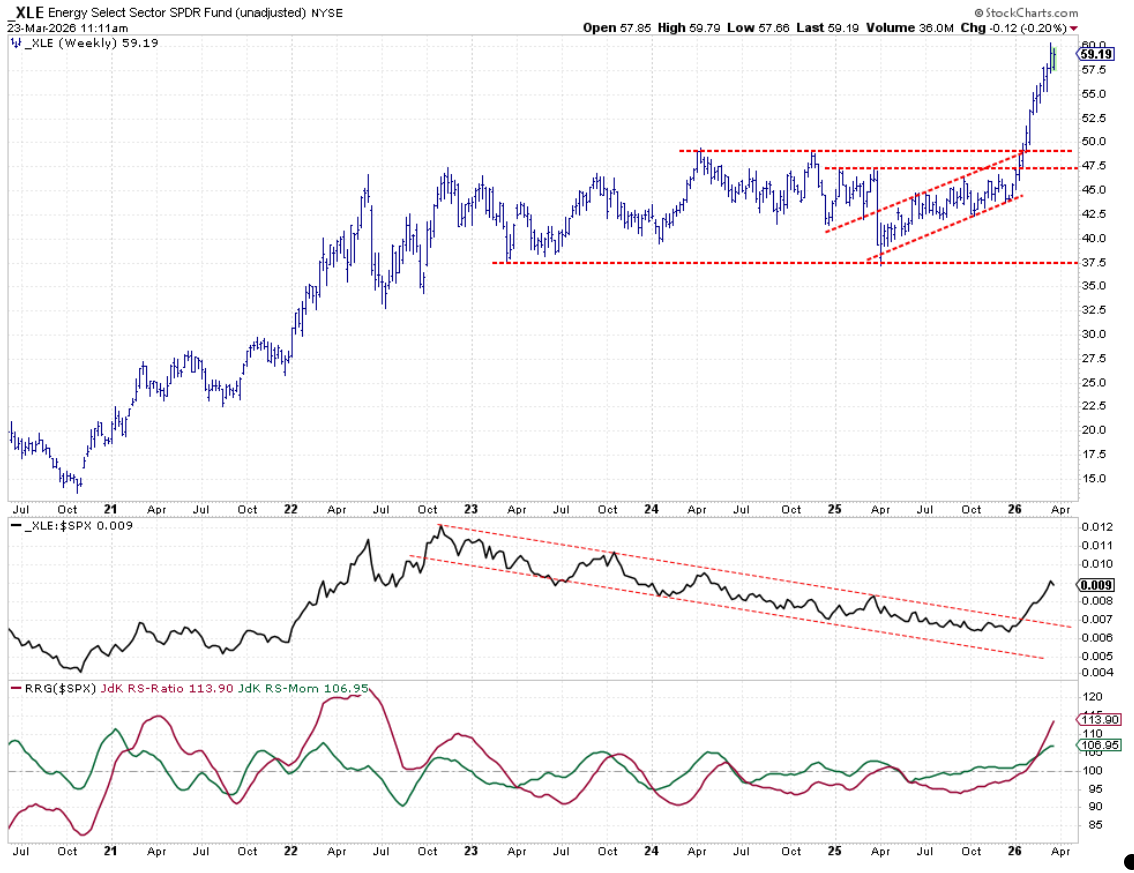

Energy

The energy sector remains robust, pushing higher even on Monday and moving toward the upper part of last week’s range. Raw relative strength is at high levels, with both RRG lines well above 100, highlighting the sector’s current strength.

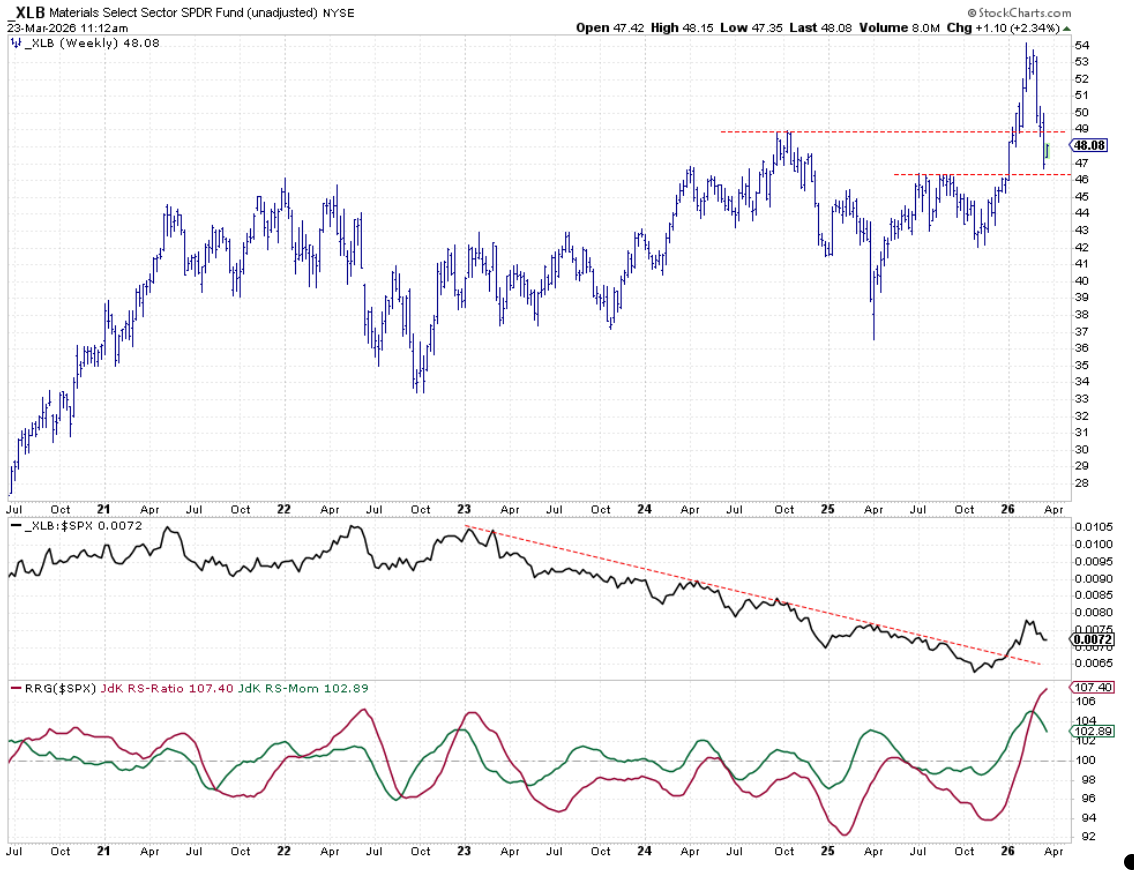

Materials

Materials dropped below its first support level (just under $49) and now rests above the second support level (around $46). The decline over the past three to four weeks has brought down raw relative strength, which could set the stage for a meaningful turnaround if a higher low forms. The RS-ratio remains high while RS-momentum has started to correct, leaving room for a corrective move without turning negative.

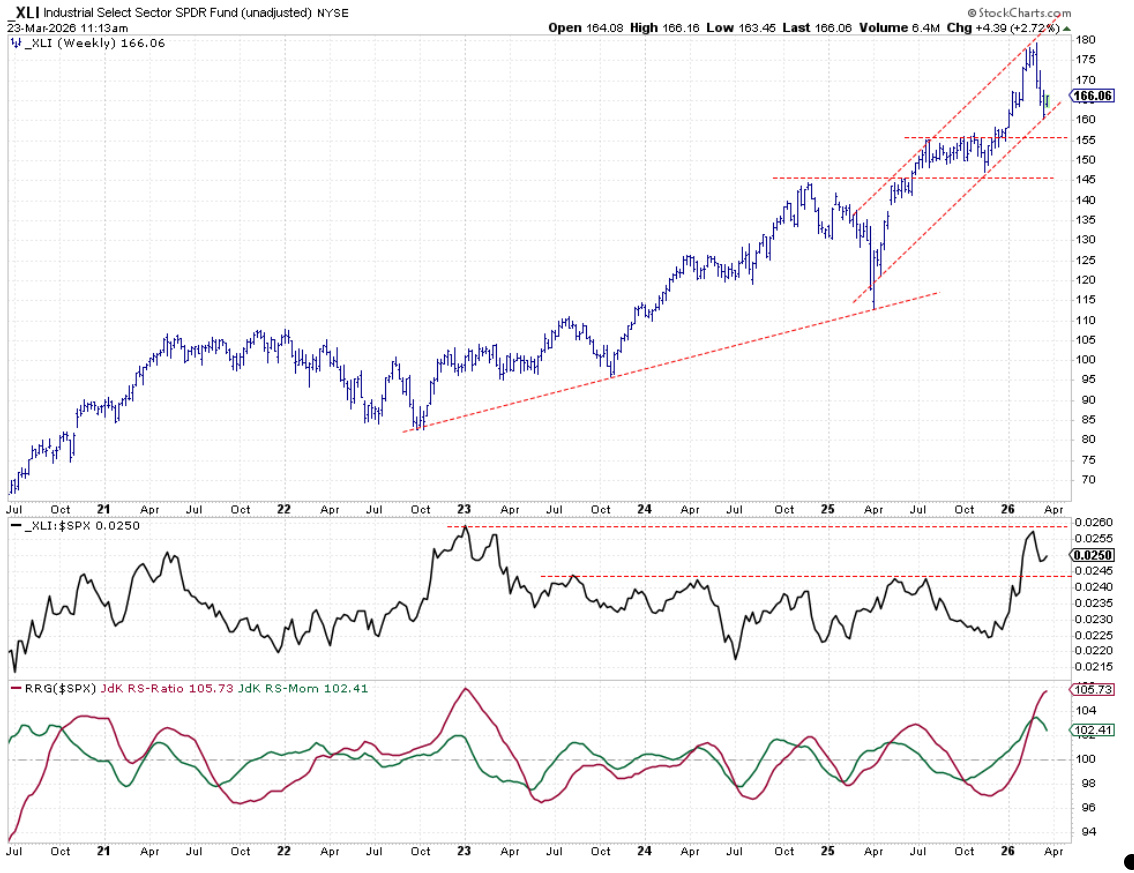

Industrials

Industrials pulled back from highs near $180, forming a low around $160, which now marks the lower boundary of a new rising channel. If this level holds, there’s upside potential within the channel.

The Raw RS line bounced lower off resistance from early 2023, but, as long as it stays above previous peaks, the sector’s outlook remains positive. A high RS-ratio and rolling RS-momentum suggest room for correction without a negative trend.

Utilities

Utilities peaked at the upper boundary of its channel and continues to move lower. Despite Monday’s uptick, the sector could drop to around $44, where intermediate support is found.

The Raw RS line is bouncing off horizontal resistance, and RRG lines haven’t been significantly impacted. Clearing overhead resistance would be a positive development.

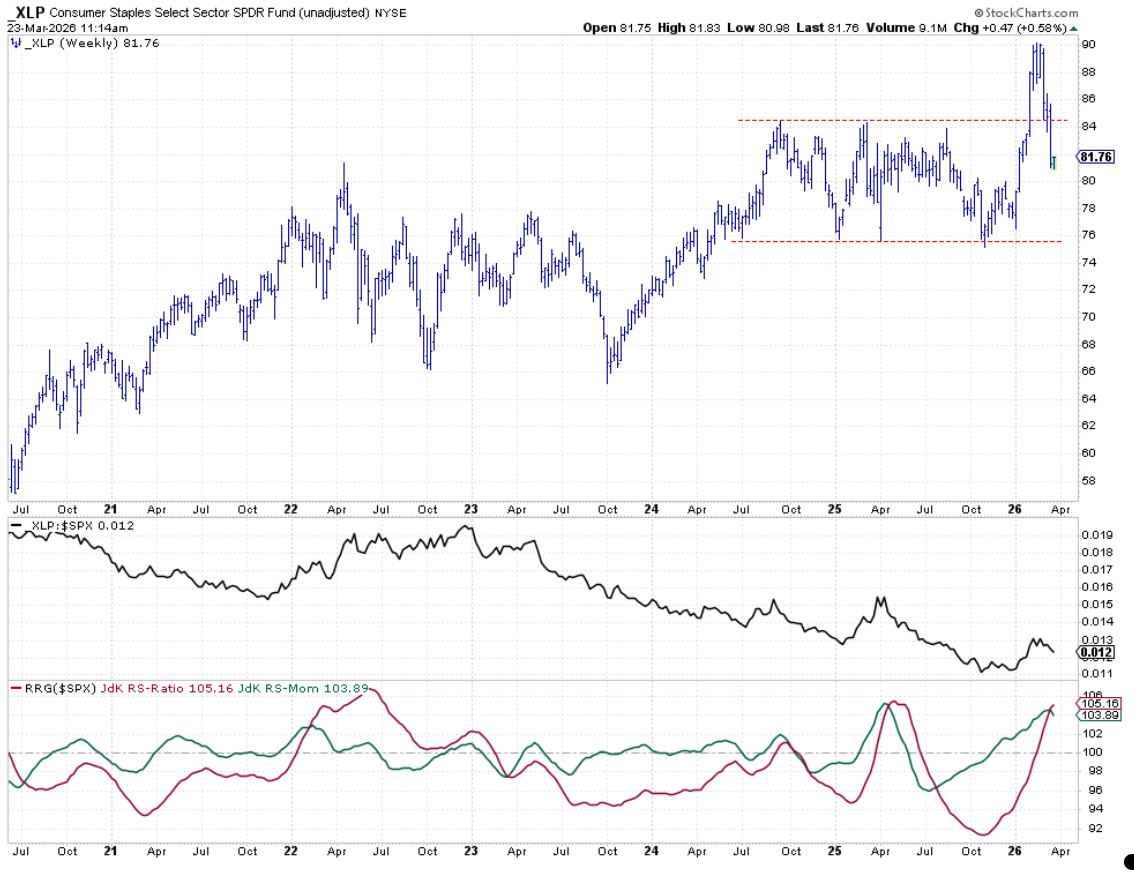

Consumer Staples

Consumer Staples unexpectedly dropped back into its old trading range, now sitting in the middle. Intermediate support is around $80, and a new higher low in the Raw RS line would be encouraging. The RS-momentum line has peaked and rolled over, suggesting a corrective move is likely, but RS-ratio levels remain high, keeping the sector in the top five.

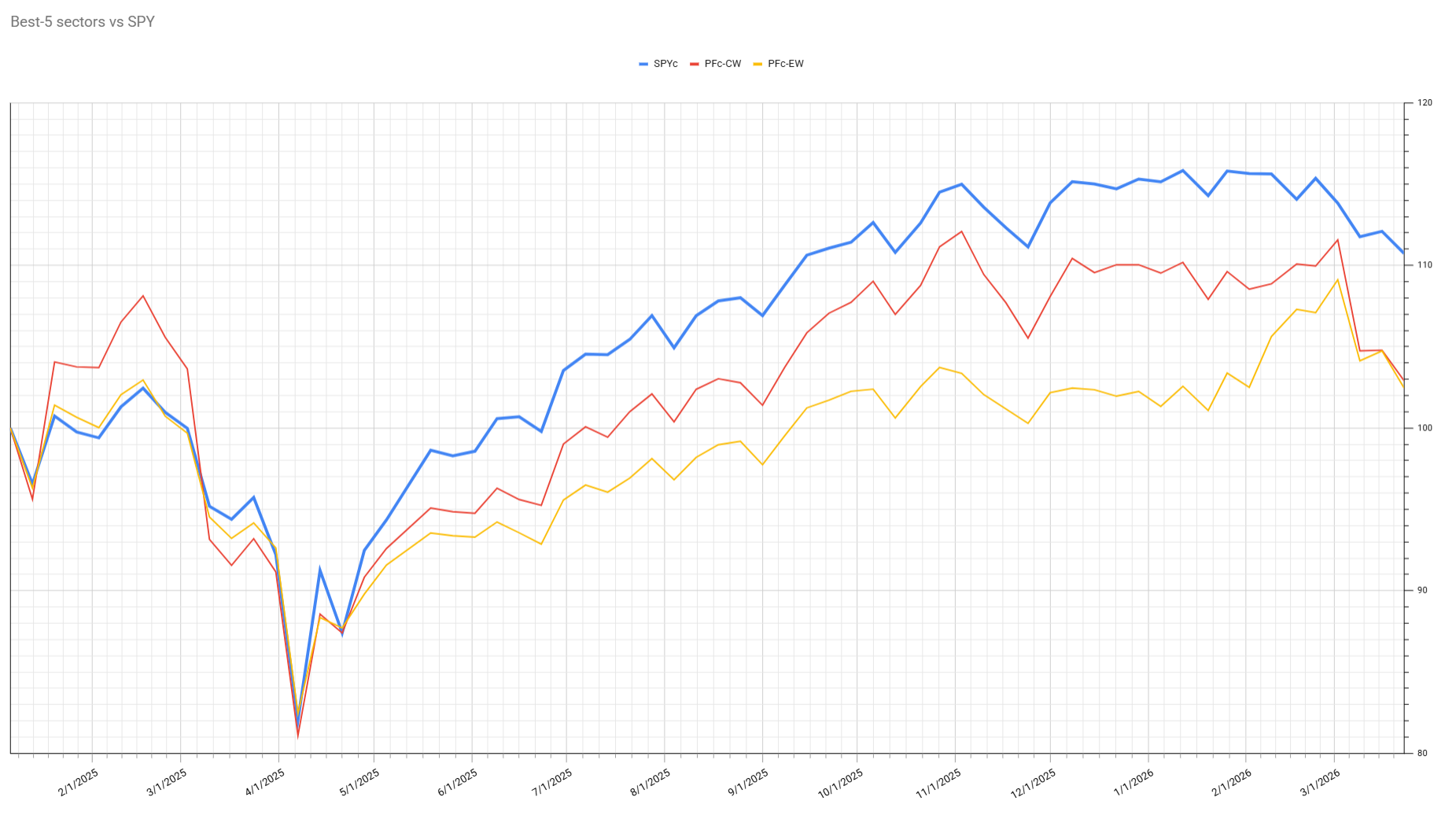

Portfolio Performance

Portfolio performance has not changed much since last week. The portfolio is now about 7% away from the S&P 500 and a new upward run is needed.

The damage from two weeks ago remains. For the portfolio to outperform, weaker general market conditions and underperformance from Consumer Discretionary, Financials, and Technology would be beneficial, given the defensive positioning.

Bottom Line

The sector rotation continues to favor defensive sectors, with Energy, Utilities, and Staples maintaining their positions at the top. While some sectors are showing signs of correction, the overall composition remains strong amid ongoing market volatility. The lagging performance of Technology, Consumer Discretionary, and Financials further reinforces the defensive bias, suggesting caution is still warranted.

#StayAlert, -Julius