A Market in Transition: Navigating Volatility and Rising Macro Risk

Last week’s market action is best understood through the broader S&P 500 ($SPX), where the headline move hides a much deeper deterioration beneath the surface.

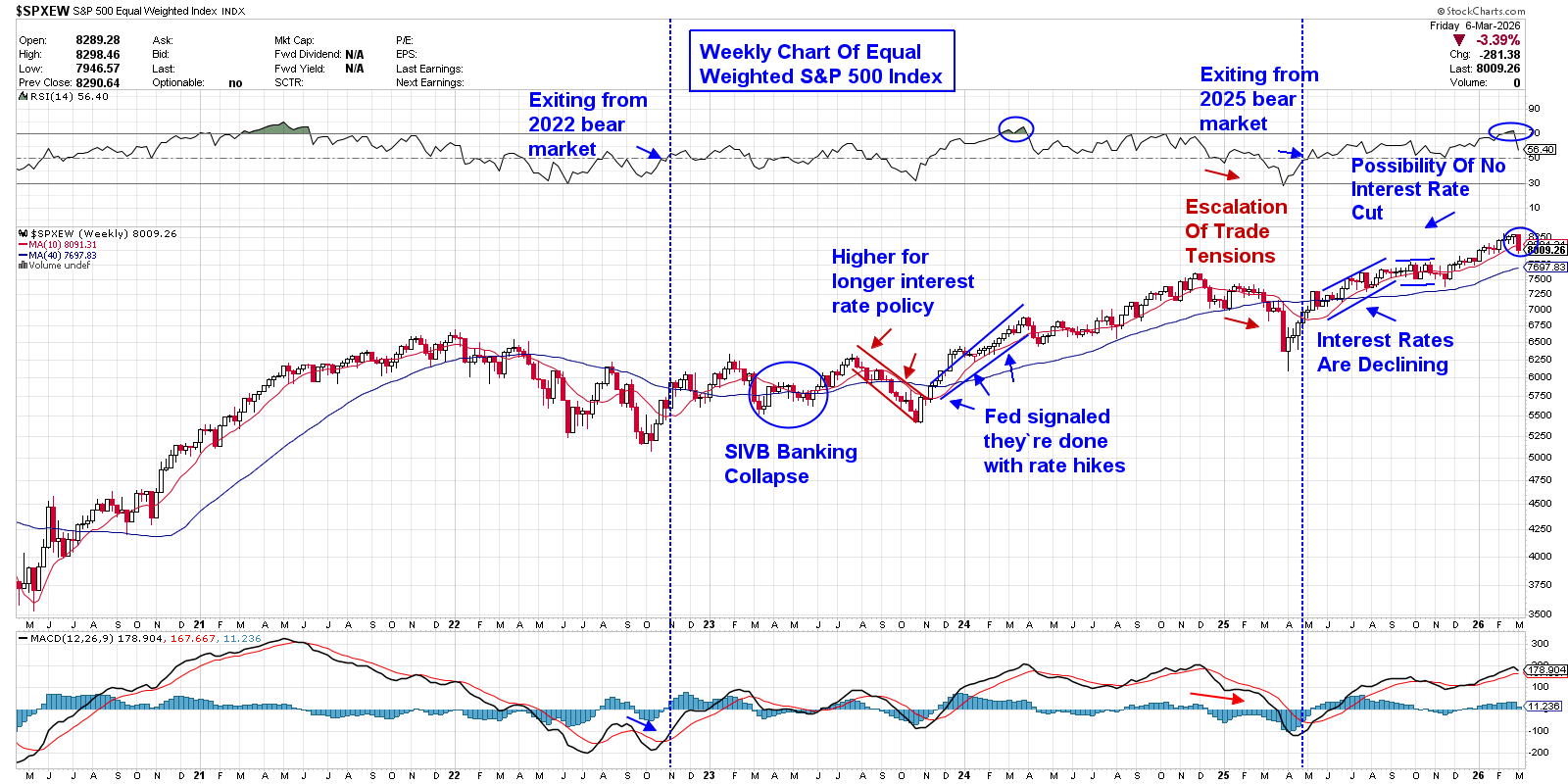

While the cap-weighted index is down 2% for the week, the S&P 500 Equal Weight Index ($SPXEW) has fallen 3.3%, confirming that the average stock is under significantly heavier pressure.

Market breadth weakened sharply as decliners overwhelmed advancers, signaling this isn’t just a handful of large stocks pulling the index lower, but a broad risk-off shift across institutional portfolios.

Sector performance reinforces that view. Ten of the 11 sectors finished lower, highlighting widespread selling as investors reduce cyclical exposure amid rising geopolitical and macro uncertainty.

At the center of the move is the deepening crisis in the Middle East. Shipping disruptions through the Strait of Hormuz have pushed energy markets sharply higher, with Brent crude oil surging to roughly $92.80 per barrel, putting crude on pace for its largest weekly gain since the early stages of the 2022 energy shock.

At the same time, the labor market delivered an unexpected negative surprise. The U.S. economy lost 92,000 jobs last month, while the unemployment rate rose to 4.4% and labor force participation dropped to its lowest level since 2021.

That combination creates a classic stagflation dilemma for policymakers. Cutting rates too quickly risks repeating the policy mistakes of the 1970s, when premature easing allowed inflation pressures to become entrenched.

Given the uncertainty, the Cboe Volatility Index ($VIX) rose 33% last week and closed at 25, which points to higher than average fear.

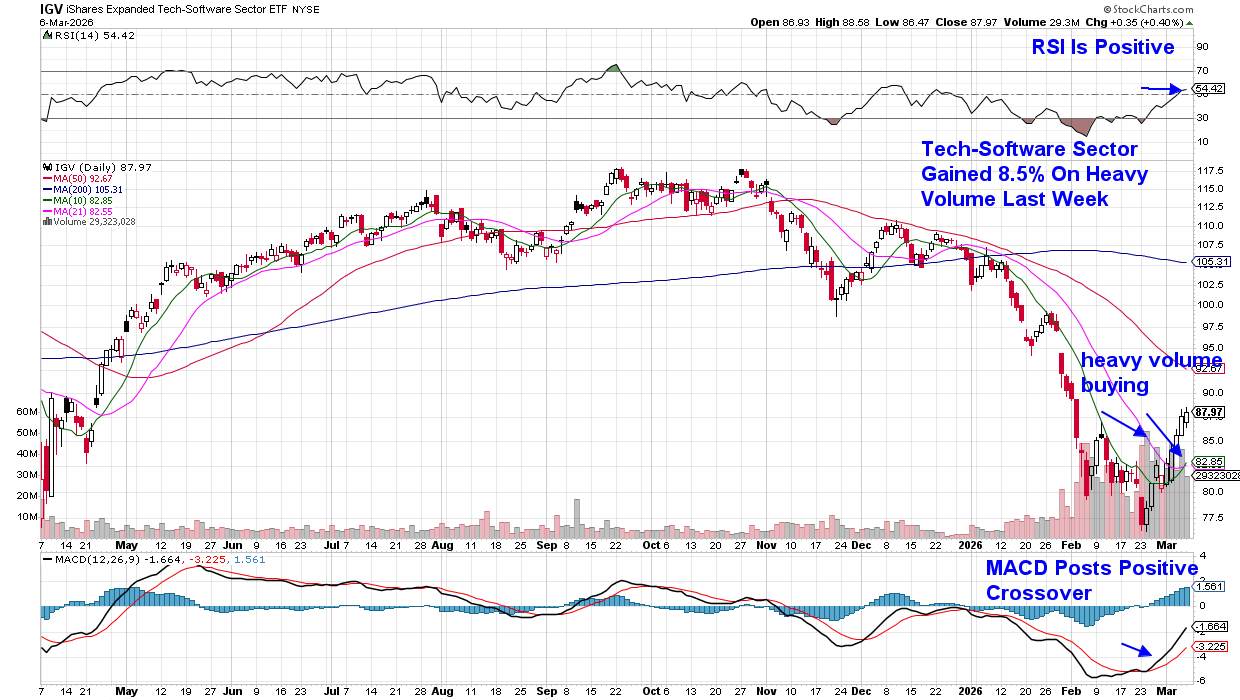

Amid the uncertainty, there was a pronounced move into beaten down Software stocks that reported better-than-expected earnings. The group had lost 26% from recent highs (using IGV), and the above average volume in these names signaled a rotation into the relative safety of lower multiple stocks.

The market is now focused on two signals — the possible duration and intensity of the Middle East conflict and, hence, the price of crude oil. If crude moves above $100, inflation risks would likely delay Fed easing and increase volatility.

Technically, the S&P 500 is now testing an important intermediate support zone, and failure to stabilize here would likely open the door to a retest of the next area of possible support.

If you’d like a detailed review of the support levels for the market, as well as the top Software stock we added to our Suggested Holdings List last Wednesday, use this link here to trial my twice-weekly MEM Edge Report at no cost. You’ll want to stay on top of these markets!

Warmly,

Mary Ellen McGonagle

Editor, MEM Edge Report