Is Distribution Hitting the S&P 500? What Traders Should Watch Now

Key Takeaways

- US large caps dipped to multi-month lows this week amid oil’s surge, but dip buyers responded.

- A subtle sector shift offers some hope for the bulls heading into key earnings reports and macro data.

- SPY distribution risk and the dollar’s consolidation are potential bellwether indicators.

Traders can finally turn away from geopolitics in the days ahead...hopefully. After the Beige Book’s release on Wednesday afternoon, Broadcom (AVGO) earnings hit the tape. The less-heralded, non–Mag 7 chip giant is like most of the others, mired in a major drawdown (-25% from its $413 December record high). Lower for four straight sessions, a bounce back would be a welcome relief for the VanEck Semiconductors ETF (SMH).

Chip & Consumer Earnings Briefly Turn the Page on Geopolitics

Then come quarterly updates from Marvell (MRVL) and Costco (COST). The former will add fuel to SMH’s volatility, while the latter offers fresh clues on consumer health.

Zooming in on the wholesale club, there are notable bullish trends after what was a dreadful back half of 2025. Recall that the Consumer Staples giant declined from $1067 last June to a 16-month low the following December. By my count, it was COST’s first set of 52-week lows going back to March 2009.

Today, though, COST is above its long-term 200-day moving average and the rising 50dma. In fact, a bullish golden cross pattern is set to occur just as its fiscal Q2 report comes out. I assert that an upside reaction would be a sanguine macro indicator. While it’s true that Consumer Staples are defensive, COST is anchored to the strength of middle- and upper-income consumers and was a secular bull-market leader.

It’s Not the Data, It’s the Reaction

Right now, we don’t want to see a pullback in that cohort, particularly as names like American Express (AXP) flash warning signs. We’ll find out not so much from the revenue and earnings numbers on Thursday night, but from the stock’s reaction on Friday. Remember: It’s how investors respond to fundamental data that matters more than the data itself.

Eco Data Grabs the Spotlight

On that note, rather than constant, concerning chatter about the war in the Middle East, a de facto closure of the Strait of Hormuz, drone and missile attacks, and the potential for $100+ per barrel WTI and Brent crude oil, Friday morning will be all about domestic economic data.

And this will be a first, by my recollection: the February Employment Situation report and the January Retail Sales report crossing the wires simultaneously. What will be the headline jobs change? Will consumer spending verify strength to kick off the year? Who knows ...

Risk Appetite on a Friday Afternoon & Sector Developments

What we will be able to discern, however, is traders’ risk appetite heading into the weekend. Price action to close the first week of the month, which included a near-30 handle on the VIX, could yield breadcrumbs on how the rest of Q1 plays out. Will it be March Madness, or will we go out like a lamb after March came in like a lion? Rather than shrugging our shoulders, let’s head to the charts.

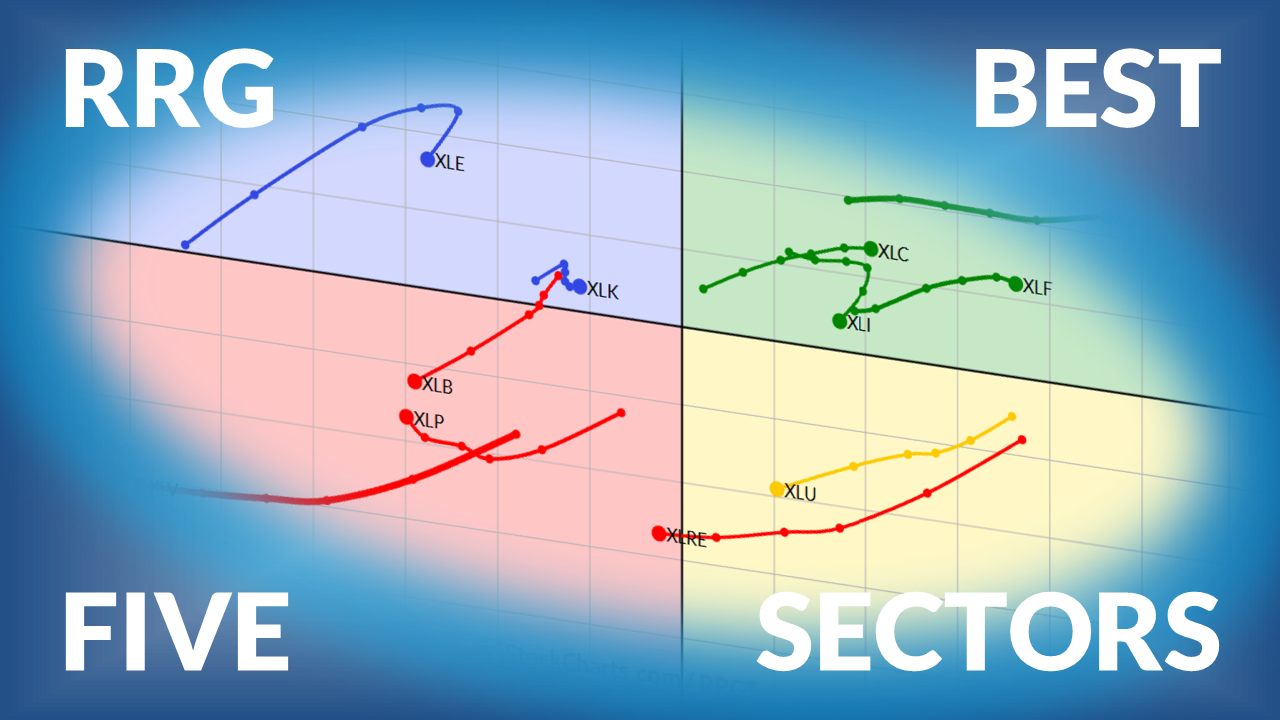

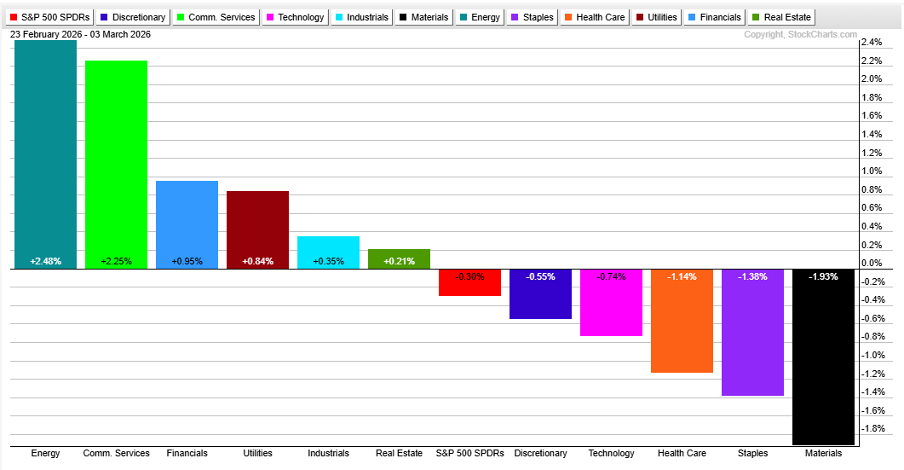

Sector trends have grabbed my attention this week. Amid intense volatility in Energy and other cyclicals, the Financials (XLF) sector has posted modest alpha. It’s a welcome development for the bulls, given that banks et al. helped lead the market since October 2022. Still, we see that Energy (XLE) and Utilities (XLU) have remained outperformers over the past six sessions.

But look at two of the laggards: Health Care (XLV) and Consumer Staples (XLP). There hasn’t been a 100% flight to defense during the VIX’s climb. To be clear, the S&P 500 (SPY) is only down fractionally since February 23, but there may be a slightly improved sector tone. We’ll know more by Friday’s finish.

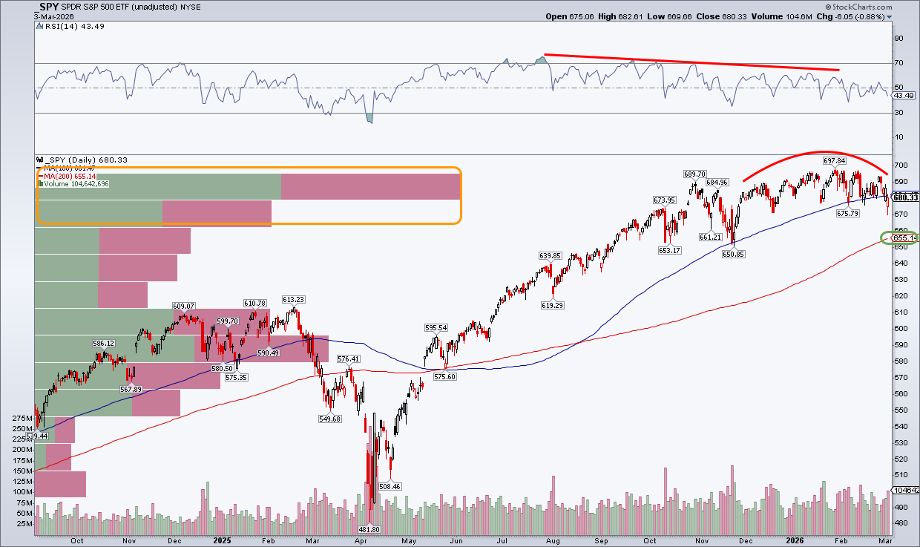

SPY: Bulls & Bears with Unfinished Business

Zooming out, SPY itself continues to look vulnerable, evidenced by a bearish rounded top in play, along with a break below the 100-day moving average. I don’t usually look at the 100-day moving average, but it has been a decent gauge of apparent support and resistance over the last two years.

The bulls have put up strong fights this week, with U.S. large caps finishing well off the lows on Monday and Tuesday. The volatile, high-volume action only adds to the substantial number of shares traded between $670 (Tuesday’s low) and the January 28 record high just below $700. One word should spring to a technician’s mind: distribution.

Generally, longs want to see tight consolidation, not patterns that play out over many months. The risk is that large traders are dumping shares over time after an uptrend. Beware the Ides of March and beware distribution signatures.

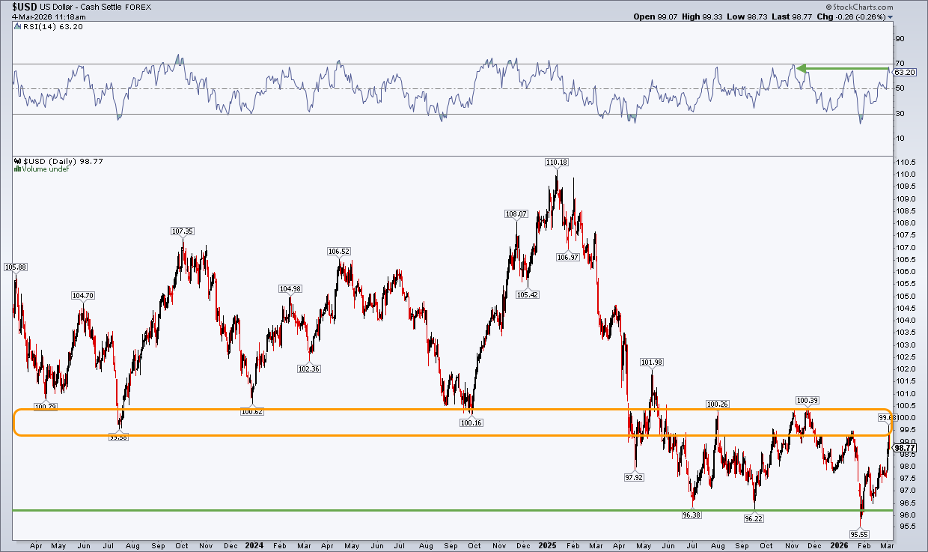

The Dollar’s Climb: What It Means Now

From an intermarket perspective, the U.S. Dollar Index ($USD) should be on your screen for the balance of the quarter. Earlier this week, it ventured into the 99.50 to 100.50 battle zone, only to be initially rejected. Back under 99 ahead of key economic data, a jump to 10-month highs (above 100.39) would likely coincide with risk-off market behavior.

The recent upswing followed a bullish false breakdown, when greenback sentiment was simply too bearish. To level-set, it’s extremely unusual to see the USD trade in such a narrow range for so long. Once a breakout or breakdown occurs, it should have major implications for global asset classes. For now, it’s a wait-and-see scenario.

The Bottom Line

March volatility arrived right on cue. Geopolitical risk spiked, but the S&P 500 isn’t giving up so fast. Notable earnings reports and impactful economic data are due soon. How markets react into the weekend will be the real tell. At the very least, it gives traders a chance to turn away from geopolitics. I’m watching sector trends, the S&P 500’s months-long consolidation, and a rangebound dollar.

Disclaimer: This blog is for educational purposes only and should not be construed as financial advice. The ideas and strategies should never be used without first assessing your own personal and financial situation, or without consulting a financial professional.