The Best Five Sectors This Week #61

Key Takeaways

- The top five S&P 500 sectors remain stable despite market volatility.

- The weekly RRG shows leading sectors maintaining uptrends, while daily RRG highlights mixed momentum across quadrants.

- Energy and Materials face short-term setbacks but retain strong relative strength.

- Defensive portfolio positioning lags the S&P 500 rally, reflecting a cautious approach amid geopolitical uncertainty.

Navigating Volatility with a Defensive Portfolio

After a robust week for the S&P 500, which gained nearly 3.5%, the composition of the top five sectors remains unchanged. Despite ongoing geopolitical volatility, the sector rankings have held steady, though this turbulence has impacted portfolio performance. As long as the rankings remain consistent, I plan to sit out the current volatility and maintain the existing strategy.

At the close of last week, the Energy sector continued to lead, followed by Materials, Industrials, Consumer Staples, and Utilities, rounding out the top five. In the lower half, Real Estate moved up from seventh to sixth place, pushing Health Care down one spot. Communication Services, Technology, Financials, and Consumer Discretionary remain at the bottom of the rankings.

- (1) Energy - XLE [15%]

- (2) Materials - XLB [10%]

- (3) Industrials - XLI [40%]

- (4) Consumer Staples - XLP [25%]

- (5) Utilities - XLU [10%]

- (7) Real Estate - XLRE*

- (6) Health Care - XLV*

- (8) Communication Services - XLC

- (9) Technology - XLK

- (10) Financials - XLF

- (11) Consumer Discretionary - XLY

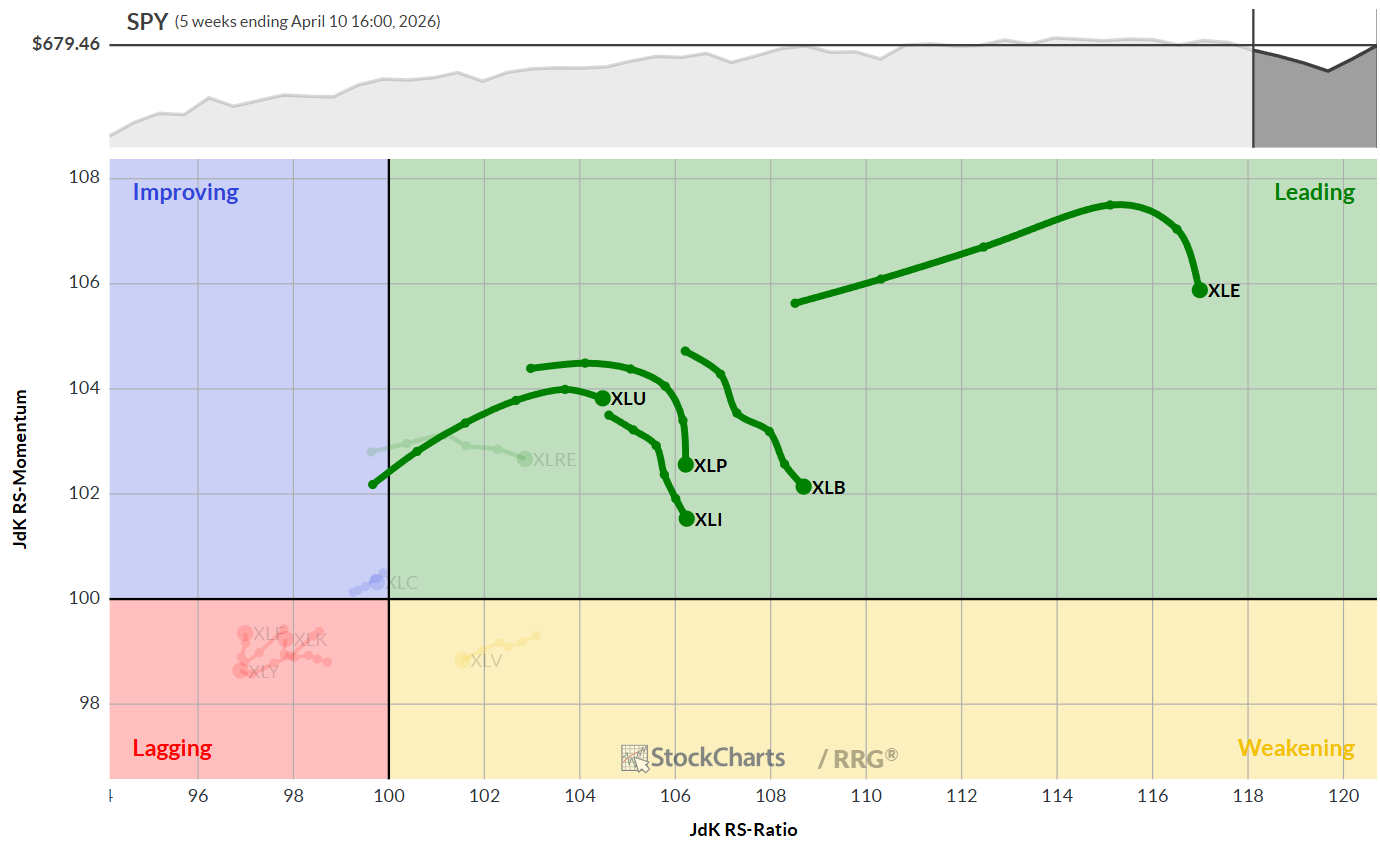

Weekly RRG

On the weekly Relative Rotation Graph (RRG), all five leading sectors are still within the leading quadrant, continuing to climb on the RS-ratio scale even as they lose some relative momentum. This suggests that their weekly relative uptrends are intact, though they are experiencing a temporary setback, especially given their elevated RS-ratio levels.

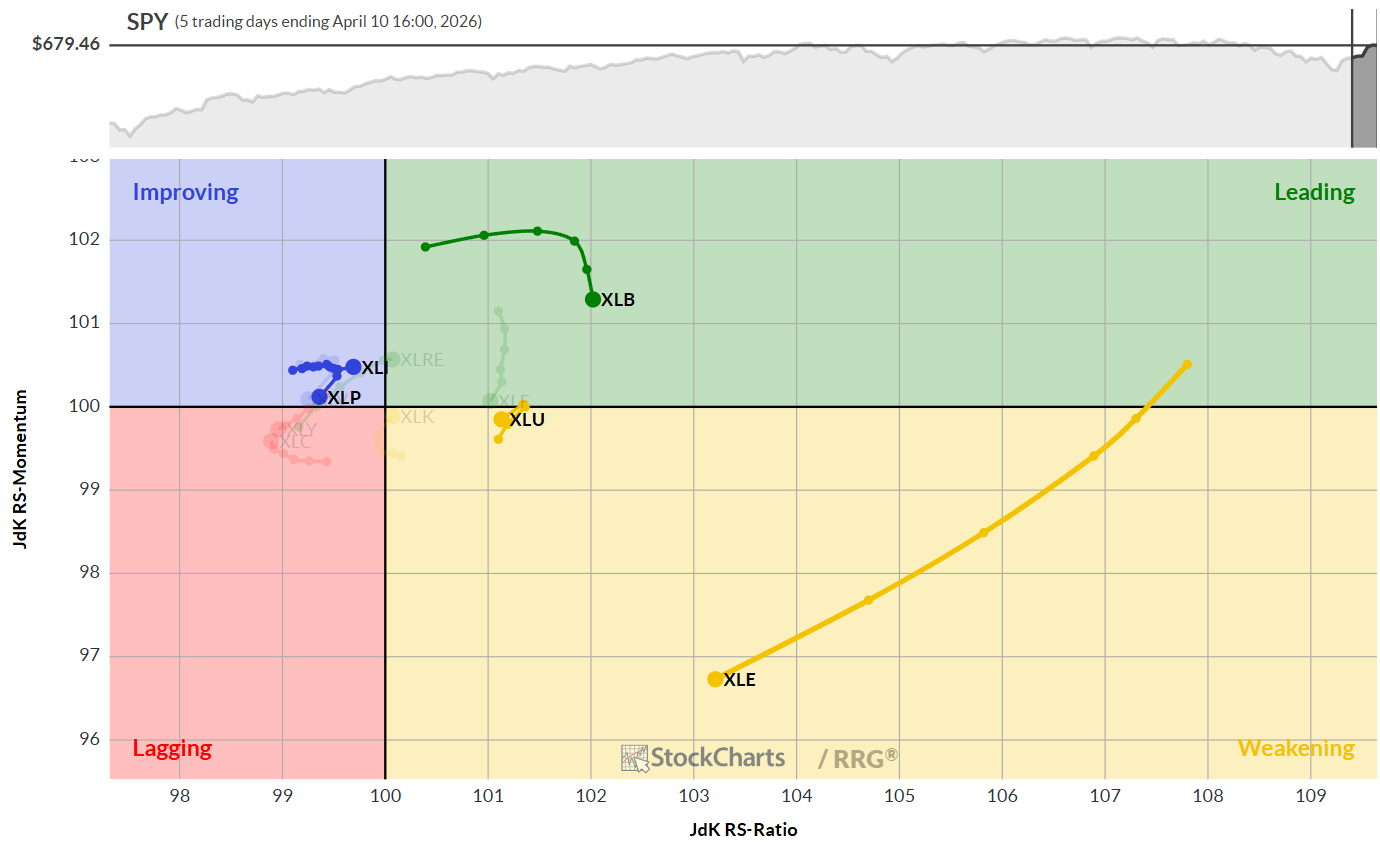

Daily RRG

The daily RRG paints a more nuanced picture, with the five leading sectors spread across three quadrants:

- Materials: Still in the leading quadrant, but showing signs of rolling over in relative momentum.

- Energy: Deep in the weakening quadrant with a long tail, rapidly losing relative momentum. Given its strong weekly performance, a significant rotation through weakening on the daily chart is not unexpected.

- Utilities: Shows a leftward hook after attempting to move from weakening to leading. The short tail indicates a stable and upward relative trend.

- Industrials and Consumer Staples: Both are in the improving quadrant, close to the center of the chart and the S&P 500’s performance. Industrials are nearly back in the leading quadrant, while Consumer Staples are rolling over toward the lagging quadrant. Both sectors are moving in line with the index.

Sector Highlights

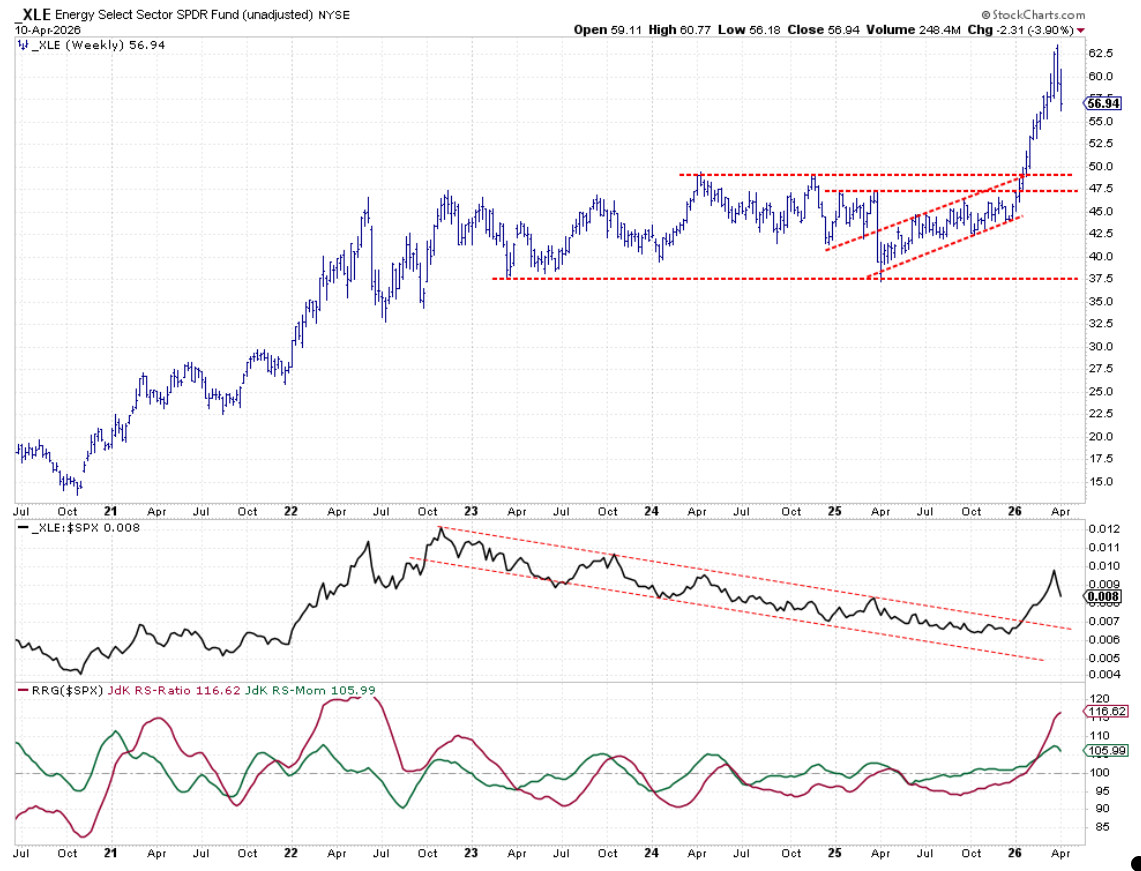

Energy

After a sharp move higher following a breakout just below $50, XLE peaked at around $62.50 and is now experiencing its first post-breakout decline. The next higher low will be crucial in assessing the sector’s underlying strength.

The relative strength (RS) line is also seeing its first setback, with RS-momentum rolling over, but the RS-ratio is still at high levels.

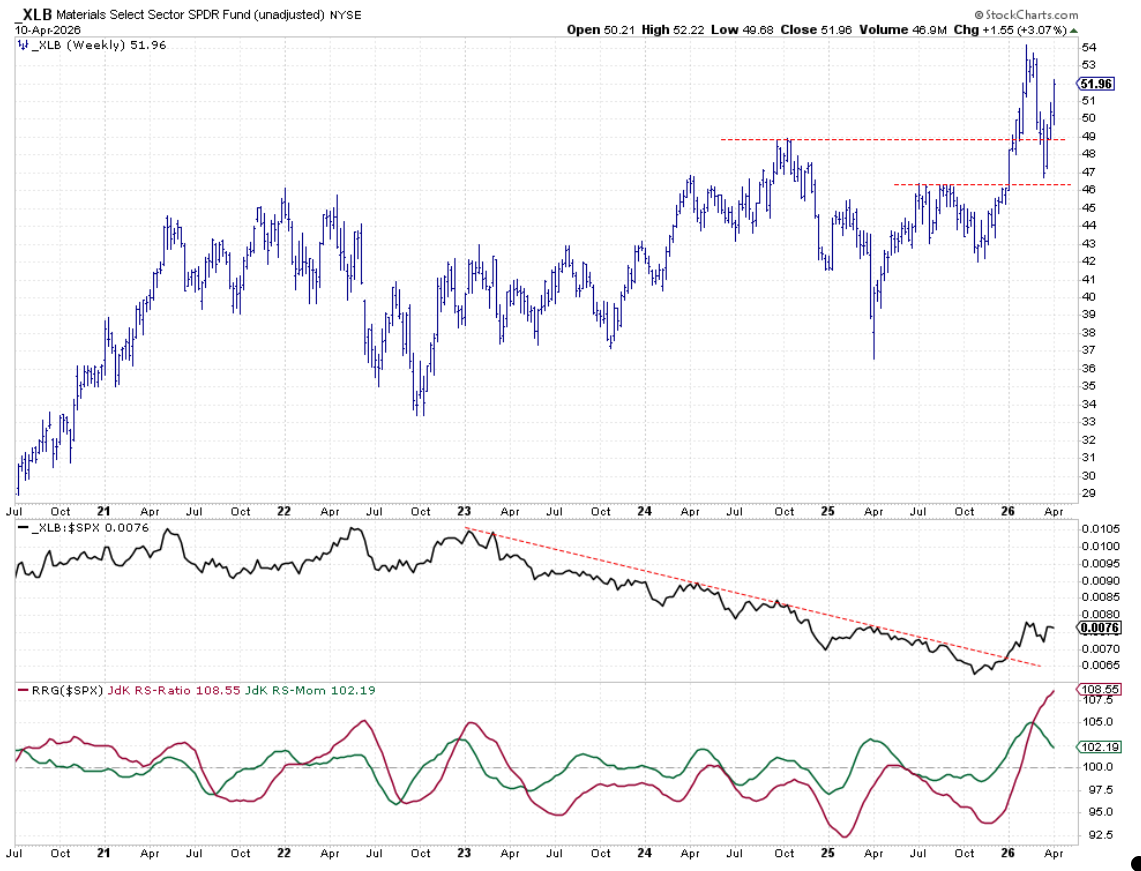

Materials

The sector established a higher low above $46, a former resistance now acting as support, and is heading back toward its all-time high near $54. The RS line also set a higher low, and a break above the previous peak would confirm the sector’s relative strength. The RS-ratio remains high, and once RS-momentum turns up again, Materials could push further into the leading quadrant.

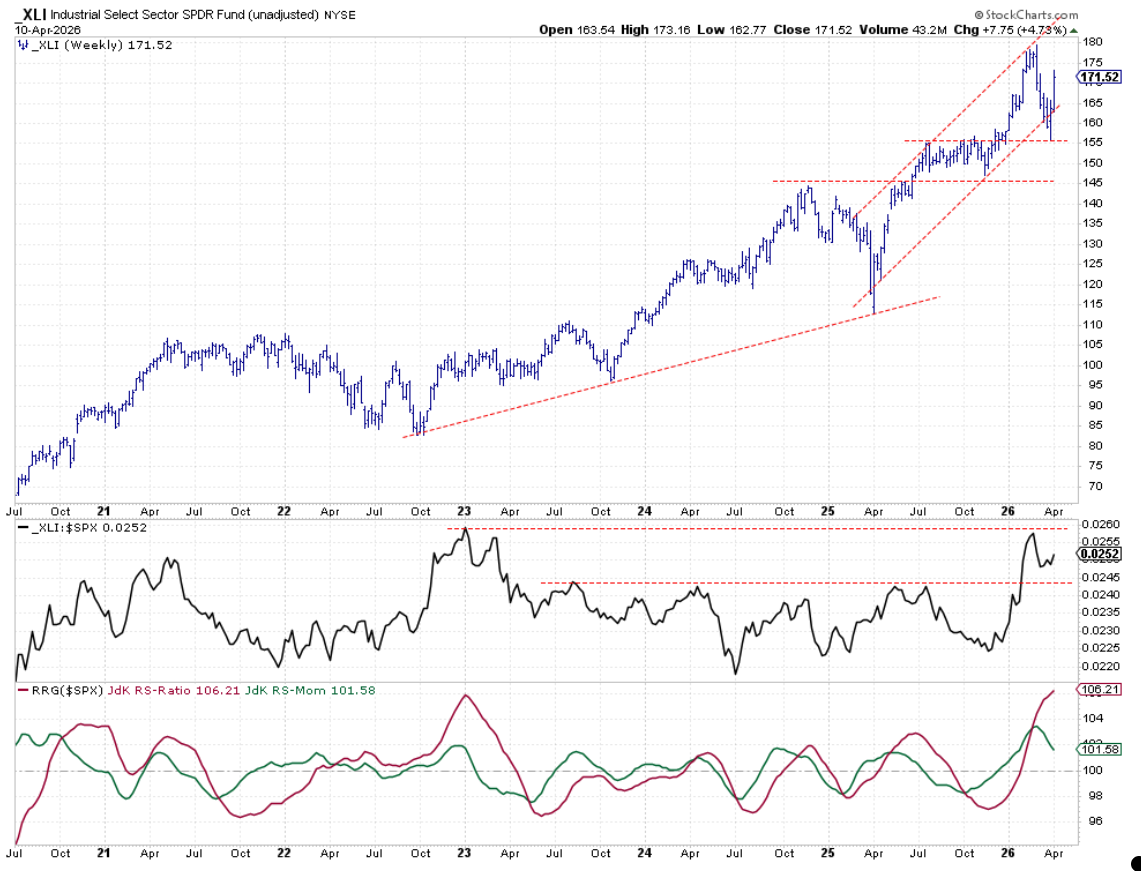

Industrials

After briefly moving out of its rising channel, industrials are back within its boundaries, setting a higher low at the previous resistance around $155. The RS line shows a peak at early 2023 levels, followed by a setback and a new higher low. Breaking above the current resistance could trigger a more aggressive rally.

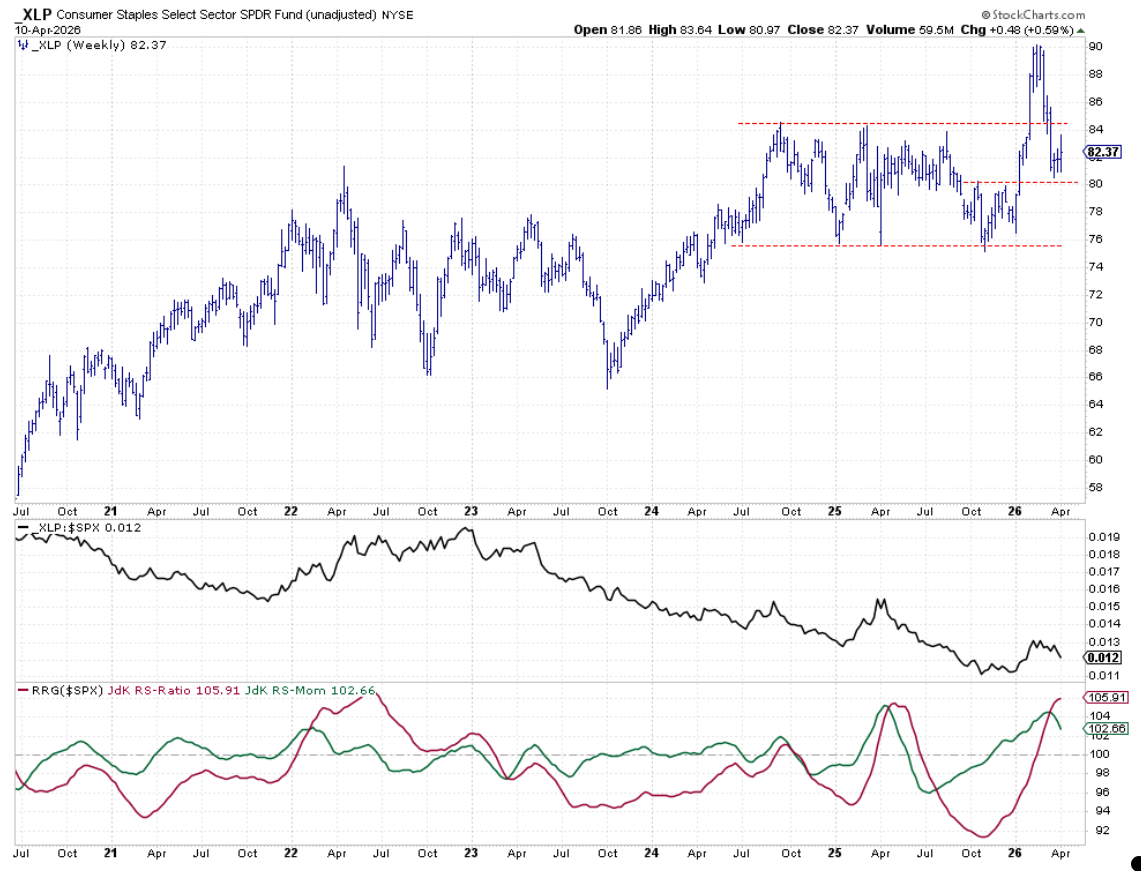

Consumer Staples

After dipping below support, Consumer Staples formed a new higher low just above $80, a previous resistance now acting as support. XLP is moving back toward resistance around $84, and a break above could lead to a renewed attempt at the all-time high near $90. However, relative strength has set a lower high, putting pressure on performance and causing RS-momentum to roll over.

Utilities

Utilities remain strong within their rising channel, with XLU pushing against previous peaks. A breakout here could unlock further upside. The RS line continues to face resistance from last year’s peaks, but both RRG lines are comfortably above 100, keeping Utilities in the leading quadrant.

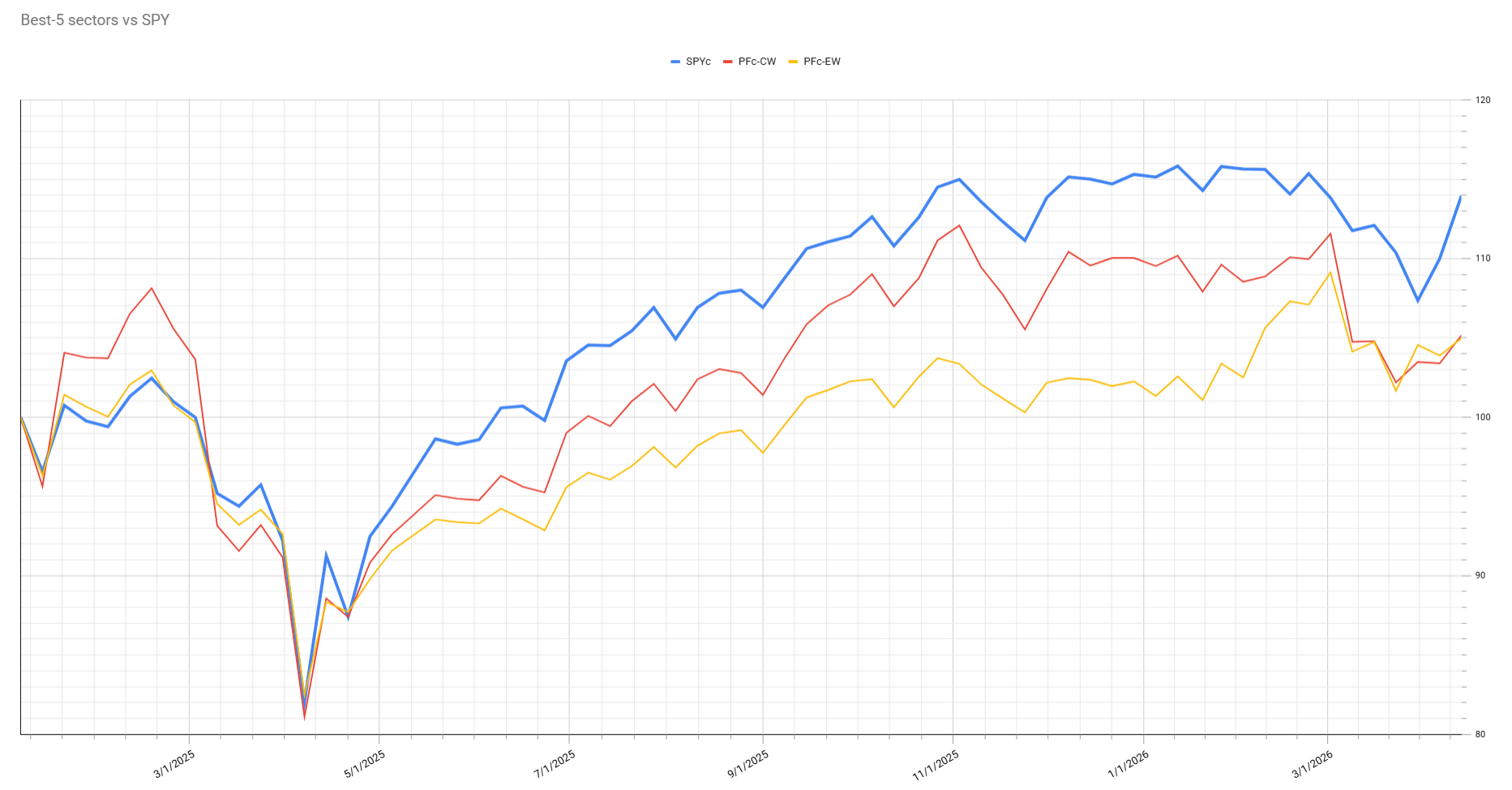

Portfolio Perspective

Last week was challenging from a portfolio perspective. The portfolio remains defensively positioned, with Energy, Staples, and Utilities dominating the top five.

As the S&P 500 rallied, this defensive stance led to a drop in relative performance, bringing us back to a 7–8% lag behind the S&P. Over the past few weeks, this has resulted in a loss of about five relative percentage points.

Despite this, the sector rankings still point to a defensive approach. Given the current geopolitical climate, unpredictability remains high.

#StayAlert, -Julius