The Bulls Controlled the First Half. Here’s What Could Change the Match

Key Takeaways

- The stock market closed the first half strong, led by semiconductors and broad strength across major indexes.

- Despite Wednesday’s pullback, the broader technical picture remains neutral to bullish, with breadth, new highs, and sentiment still supportive of bulls.

- The U.S. dollar/Japanese yen, Middle East peace talks, and upcoming Fed rate decisions could be the major players in the second half.

It was a strong first half for the stock market. The bulls went into halftime with a comfortable lead.

After Tuesday’s close, the big headline was that Q2 marked the best quarter in six years for the Nasdaq Composite ($COMPQ), the Nasdaq 100 Index ($NDX), S&P 500 ($SPX), and VanEck Semiconductor ETF (SMH). Considering the recent pressure in technology stocks, the data served as a reminder that things weren’t nearly as weak as they may have felt.

Tuesday’s strong rally to month-end and quarter-end gave investors plenty to feel optimistic about. Semiconductors showed they still have leadership strength and helped drive the broader market higher. Record semiconductor shipments from South Korea may have added to the upbeat tone around the industry group.

Second-Half Kickoff

The second half of the year, however, didn’t begin with the same enthusiasm. Technology was the weakest-performing S&P 500 sector on Wednesday, and SMH pulled back more than 5%. Still, the uptrend in the daily chart remains intact, as you can see in the chart of SMH below.

The ETF has fallen below the 650 level, which marked the June 15 and June 25 highs, and is trading at its 21-day exponential moving average (EMA). Volume rose above the 50-day MA, which is a little concerning.

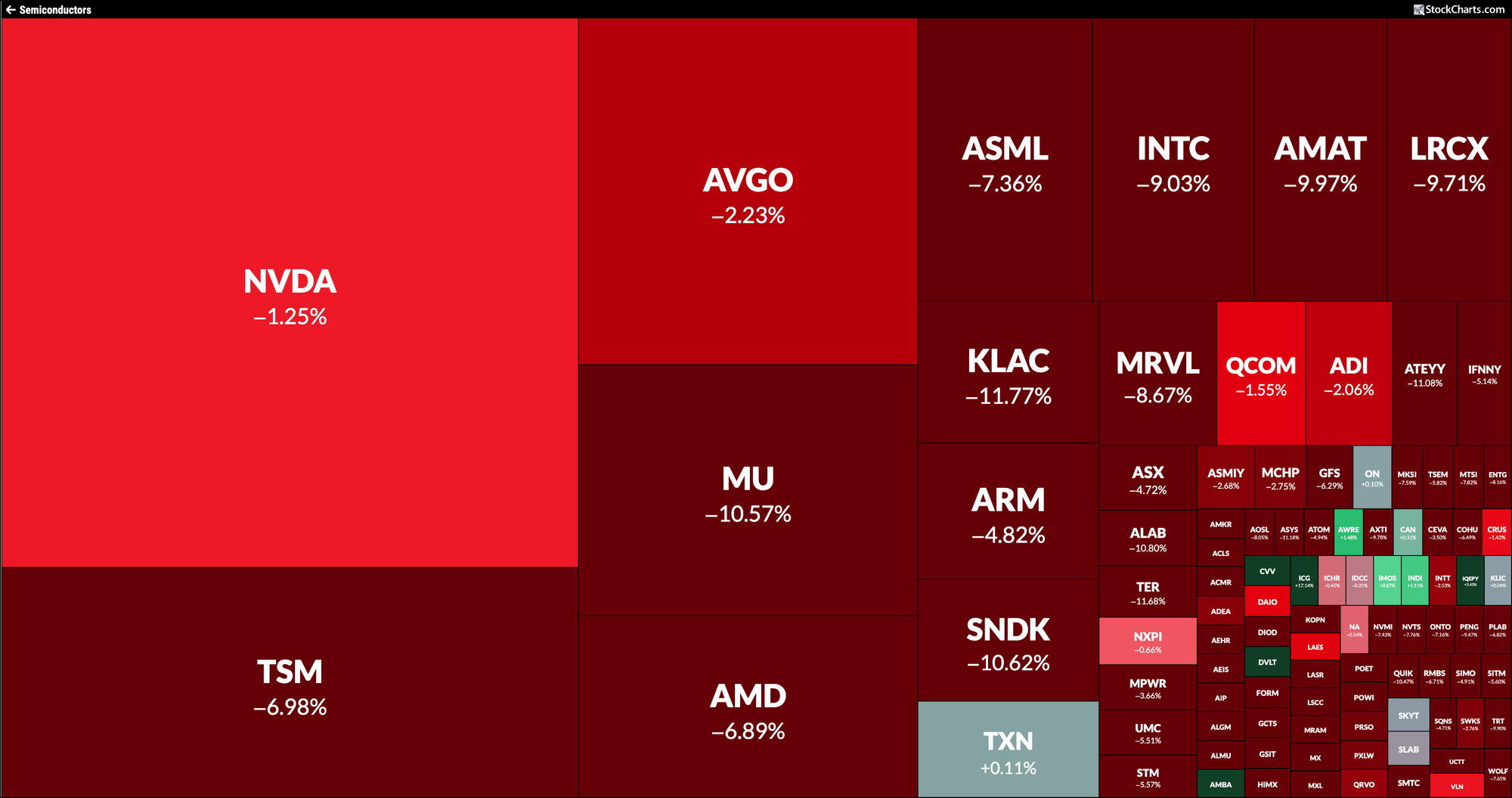

Let’s step back and visualize the semiconductor group’s second-quarter performance on the StockCharts MarketCarpets. It’s hard to miss the sea of green, led by the large-cap, heavily-weighted stocks that had a strong quarter.

Looking at the group’s overall performance, NVIDIA (NVDA), the largest cap-weighted stock, gained 21.28% for the quarter. It’s impressive, but relative to the other stocks in the group, the gain is relatively modest. There’s very little red on the carpet, and most of it is concentrated in the lighter-weighted stocks.

The MarketCarpet below shows the one-day change in semiconductors for Wednesday.

Those same stocks that helped pull the market higher during the second quarter were the ones that dragged semis lower on Wednesday. Micron (MU), Intel (INTC), and Applied Materials (AMAT) all traded sharply lower. The key is how these stocks behave around their 21-day EMAs; Micron has already reached that level. If these stocks stabilize and turn higher, the pullback could end up looking more like a buy-the-dip opportunity.

Outside of tech, the Dow Jones Industrial Average ($INDU), S&P 600 Small Cap Index ($SML), and the S&P 400 Mid Cap Index ($MID) all closed lower after hitting record highs on Tuesday. Meanwhile, the Invesco S&P 500 Equal Weight ETF (RSP) closed at a record high on Wednesday, indicating that interest in equities hasn’t waned.

A run through the Market Summary page after the close shows that market breadth is still mostly neutral to bullish, new highs outnumber new lows, and investor sentiment is bullish. Wednesdays’ top-performing industry group was Regional Banks. The Financials sector was the second best S&P 500 sector performer.

So, even though the second half got off to a less inspiring start, nothing appears to be falling apart from a technical perspective.

Outside of Equities

Light Crude Oil ($WTIC) is now trading below $70 per barrel and filled the February 27/March 1 gap up. Investors are hopeful that the U.S. and Iran come to an agreement over the ongoing conflict.

The Japanese yen has also weakened sharply against the U.S. dollar and is now trading below its July 2024 low, as you can see from the chart below (from Market Summary > Other Assets > Currencies). With the yen this weak, there is the risk of intervention. We saw this play out in July/August 2024, when the yen reversed sharply, and equities sold off. There’s a chance something similar could happen again, which makes the yen worth watching even if you don’t trade currencies.

The U.S. dollar continues to strengthen, helped by the rising expectations that the Fed could raise interest rates as early as September.

On Thursday, investors will get the June non-farm payrolls (NFP) report. If the number comes in stronger than expected, the dollar could push even higher and potentially increase the odds of a rate hike at the next Fed meeting. A stronger dollar could also place more pressure on the yen, raising the risk of intervention even further.

Right now, the dollar is in an uptrend, and is trading well above its 200-day SMA. The Relative Strength Index (RSI) is just below the 70 level, which indicates that momentum is strong but approaching overbought territory. A stronger-than-expected NFP could push the dollar above 101.60 level.

The Bottom Line

As the second half of the year begins, investors should keep a close eye on the U.S. dollar/Japanese yen, the progression of peace talks in the Middle East, and the Fed’s interest rate decisions. For now, my bias remains bullish, until the charts give a clear reason to think otherwise. What’s your bias?

Markets shift fast. If you want to stay informed without refreshing charts all day, the Market Summary page keeps you grounded.

Disclaimer: This blog is for educational purposes only and should not be construed as financial advice. The ideas and strategies should never be used without first assessing your own personal and financial situation, or without consulting a financial professional.