Can AI Stocks Continue Higher Under a More Hawkish Fed?

One of the biggest questions investors face right now is whether AI-related stocks can keep climbing if incoming Fed Chair Kevin Warsh follows through on his intention to make monetary policy more data-dependent while potentially keeping interest rates higher for longer.

The answer rests on two key variables: interest rates and earnings growth.

Higher rates can pressure growth stock valuations, but history shows that strong earnings growth can offset that headwind. The challenge arises when rates move higher as investors begin questioning future growth prospects.

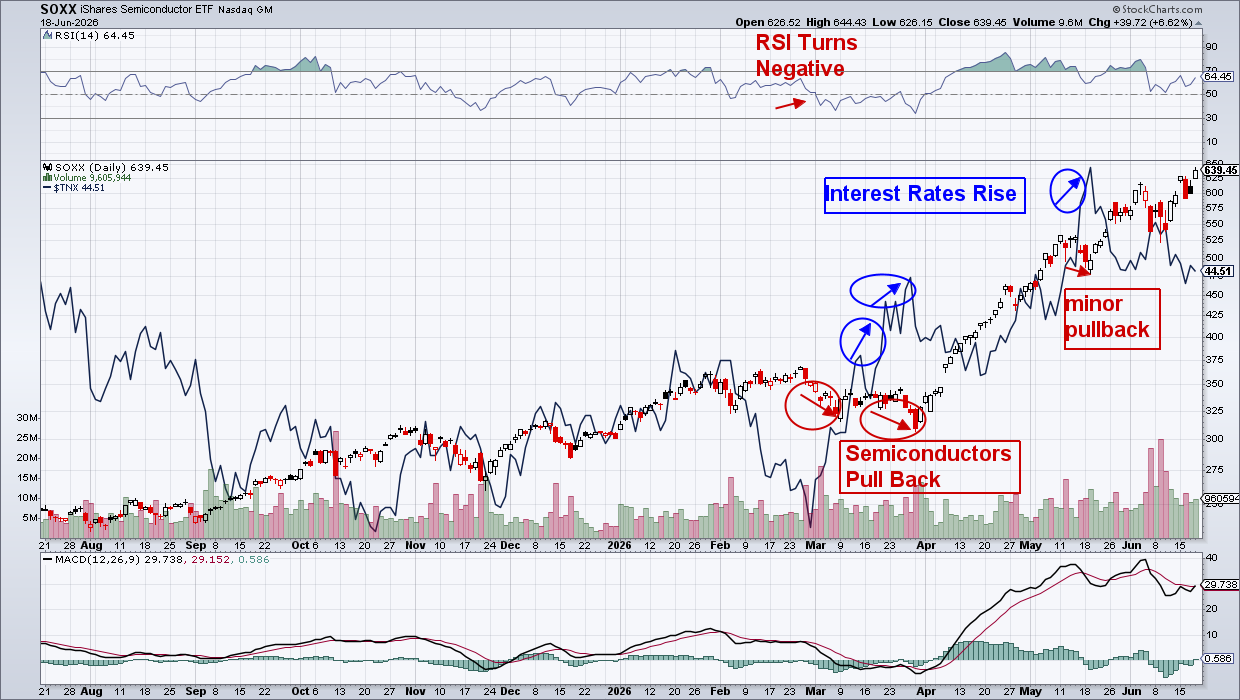

That is exactly what happened earlier this year. As Treasury yields climbed in March, investors began to reassess whether AI spending growth could continue at the pace that had been priced into many semiconductor and infrastructure stocks. The result was a sharp pullback across the group.

It wasn't simply rising rates that drove the decline. It was the combination of rising rates and concerns that growth expectations may have become too optimistic. That distinction is important. The AI trade can remain intact as long as avenues of growth remain visible. We saw this in May, when the pullback in SOXX was much less severe than in March despite a rise in rates.

In May 2026, the AI sector was dominated by massive infrastructure, distribution, and enterprise deals. The arms race shifted heavily from model-building to securing immense compute capacity and distribution channels. I highlighted this in my twice-weekly MEM Edge Report, and we stayed with our top-performing AI stocks.

However, if spending growth begins to plateau while rates remain elevated, valuations could come under increasing pressure.

Three Areas Investors Should Monitor Closely

With that in mind, investors should focus on three key indicators.

The first is Treasury Yields. The 10-year Treasury yield remains one of the most important gauges for growth stock valuations. A sustained move higher would likely pressure technology shares.

The second is AI Spending Trends. Continued spending by hyperscalers and enterprises remains critical to supporting demand across semiconductors, memory, networking, and data center infrastructure.

The third is Earnings Revisions. This is perhaps the most important indicator of all. As long as analysts continue raising earnings estimates, AI stocks can remain resilient despite higher rates.

The bottom line is that rising rates alone don’t typically end bull markets. More often, bull markets come under pressure when investors begin lowering their expectations for future growth.

Why Warsh Matters

Perhaps the most significant takeaway from Warsh's recent comments isn't the prospect of higher rates but, rather, the elimination of forward guidance.

Markets have historically adapted to higher rates. What they struggle with is uncertainty. A more data-dependent Federal Reserve means investors will have less visibility into future policy decisions, increasing the likelihood of volatility as markets react to each economic report.

To be kept up to date on broader market conditions as well as stocks benefitting from new technologies related to AI, use this link here for a no-cost trial of my top performing newsletter. It is released on Sundays and Wednesdays and provides insights not seen elsewhere.

Warmly,

Mary Ellen McGonagle

MEM Investment Research