Gold, Silver, and GDX: Are Precious Metals Ready for a Comeback?

Key Takeaways

- Oil’s surge and rising Treasury yields spelled doom for the precious metal trade earlier this year.

- Following the January melt-up, gold and silver bears have ruled price action.

- Sub-$80 WTI & Brent are bullish, but metals and gold miners face trouble from elevated real interest rates.

Elon Musk scored a big goal last week. Shares of SpaceX (SPCX) made it through the proverbial Group Stage, rallying from near $150 to above $200 in the first handful of trading days. Indeed, the market’s pitch looks a bit different today, given the Industrials sector stock’s large position in the U.S. Total Market Index.

SPCX will be added to select Vanguard index ETFs by the close of the week but, due to the small free float, holding sizes will be modest. Traders must monitor their own risk levels, however, as SPCX’s implied volatility is above 100% heading into the holiday weekend.

The Bigger Story: A Shifting Intermarket Backdrop

SpaceX is just one story, though. Investors are well served by zooming out and assessing the macro landscape. With WTI and Brent crude oil below $80 and the market discounting some semblance of a Middle East truce, intermarket trends could be shifting.

Consider the stubborn inflationary relationship between commodities and interest rates. Intermarket Analysis 101 says the two move together, and we’ve seen that since early March… at least with energy and agricultural resources.

As the broad commodity complex has come off the boil this month, precious metals have been able to put in a floor. Recall gold and silver’s dreadful price action since their January highs, amid rising real interest rates and momentum decompression following a parabolic run-up to start the year.

Having been left out of the war-induced rally, is now the time to go overweight the shiny metals once again? Let’s turn to the charts.

Gold Bulls Still Have Work to Do

Starting with gold, the bulls clearly have wood to chop. Notice in the chart below that the metal remains below its long-term 200-day moving average, and a death cross is very likely in the next few weeks. What’s more, the falling 50-day moving average marked a selling point on three occasions in April and May. I’d like to see price rally through that short-term trend-indicator line before turning bullish.

Also take a look at the RSI momentum oscillator at the top of the chart. It ranged in a weak zone between 25 and the low 50s, which also points to a defensive posture. On the plus side, there is a chance of a bullish false breakdown this month, when gold briefly dipped below the March low of $4,099, but the snapback has not been a very strong face-ripper.

Bigger picture: support has emerged in the $4,000–$4,100 area, which is key, as that’s the 38.2% Fibonacci retracement of the late-2023 to early-2026 rally.

Silver Looks a Bit Better

Silver is marginally more constructive. It held its March low earlier this month and is above its 200-day moving average. A fake-out move from just above $70 to almost $90 in late April and early May stung, but, so long as $61 holds, a further bounce is possible.

For both metals, plenty of “dead bodies” linger above current prices.

The “Real” Problem

What’s keeping gold and silver from returning to their 2025 glory? It might be the run-it-hot economy. Surging oil prices no doubt put upward pressure on nominal Treasury rates over the back half of Q1. Since mid-May, though, TIPS yields have been jumpy.

Precious metals can be driven by many macro factors, but real yields are often near the top of the list.

Why Gold Miners Could Benefit

Stronger economic growth prospects with lower energy prices are a better setup for asset-heavy gold miners. Shares of the VanEck Gold Miners ETF (GDX) are up a firm 18% from their June low, returning to the 50-day moving average this week.

Like the physical commodity, a bearish death cross is absolutely in play soon, but GDX’s false breakdown appears more constructive. A weekly close above the 200-day moving average would be encouraging, and improved relative strength this summer would be welcome.

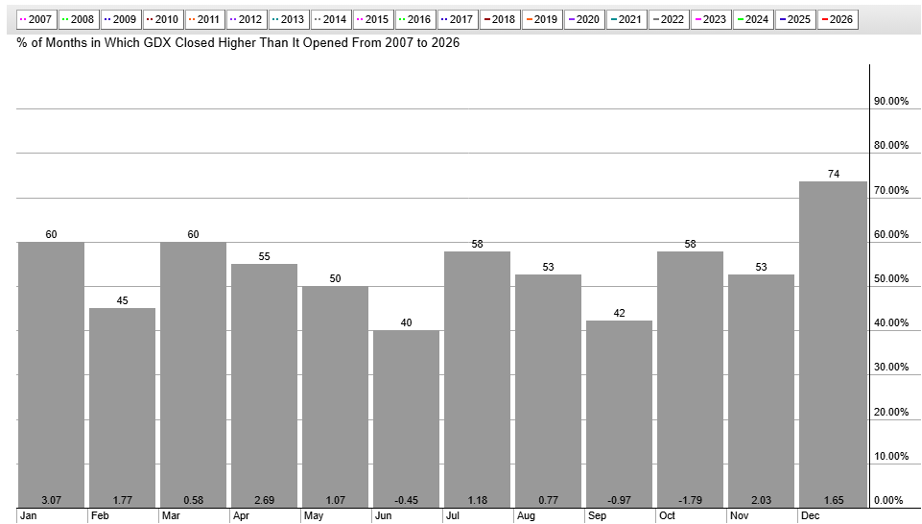

Seasonal Tailwinds Ahead

As the S&P 500 begins one of its worst two-week seasonal periods of the year, July and August have tended to be quite strong for GDX. The average July gain from 2007 to 2025 was 1.2%, followed by a 0.8% August advance.

As for the chart, GDX was up four consecutive sessions heading into Fed Day, outperforming the SPX each time. Implied volatility as of Tuesday’s close was not that high at just 44%, so traders were not anticipating fireworks after Fed Chair Kevin Warsh’s first rate-decision announcement and press conference.

What Could Spark the Next Move?

All told, the macro and intermarket conditions are coming together for gold miners. I assert that the real-rate backdrop is not all that conducive to precious-metal gains akin to what momentum traders enjoyed in 2025, but the miners can work in this environment.

I’ll be watching economic data, as any inklings of a soft patch in the labor market could be rocket fuel for gold and silver, since that could result in lower real rates. Recall that the past two summers have featured employment hiccups and a small bid to Treasuries (and prompting the Fed to lower its policy rate).

The Bottom Line

File gold, silver, and precious-metal equities as dark horses heading into midyear. Lower oil is a good thing, but the bond market isn’t cooperating quite yet. Technical damage was done from January through April, and both absolute and relative strength need to perk up more before a portfolio overweight makes sense.

Ready to see the market through a wider lens? Head to the Market Summary page and dive into the Intermarket Analysis panel for a real-time read on stocks, bonds, commodities, oil, gold, and the dollar — all in one place.

Disclaimer: This blog is for educational purposes only and should not be construed as financial advice. The ideas and strategies should never be used without first assessing your own personal and financial situation, or without consulting a financial professional.