Lower Oil, Lower Treasury Rates: What Charts Say About What the Fed Faces This Week

Key Takeaways

- The market gives Kevin Warsh a break (for now) as the macro backdrop cools.

- One key inflation measure ticked to multi-week lows, despite CPI’s recent surge.

- Strength in rate-sensitive and cyclical sectors suggests Goldilocks is not off the table.

From SPCX last week to FOMC this week. Last Friday felt like a coronation of what is now the sixth-largest domestic public stock by market cap, and positive apparent developments over the weekend between the U.S. and Iran triggered a gap higher in Sunday night futures trading. WTI crude oil traded with a $79 handle by early Monday, which is the sight now greeting Fed Chair Kevin Warsh as he and 11 other Fed voting members decide interest-rate policy this Wednesday.

It’ll be another active week for markets; in fact, it already has been. Retail Sales data prints Wednesday morning ahead of the two-day FOMC gathering, and it’s an options expiration week. Positioning will be compressed, too, given the market holiday on Friday.

A Surprisingly Calm Welcome for Warsh

But for Chair Warsh, he has been greeted with a rather friendly handshake thus far, despite plenty of ink being spilled about how the market tends to test new Fed chiefs sternly. Macro predictions and opinions aside, the TIP:IEF market-based inflation gauge retraced half of its November 2025-to-May 2026 ascent.

Since his confirmation hearings, real rates have done the heavy lifting, suggesting that economic growth (not inflation) was the Treasury market’s zeitgeist.

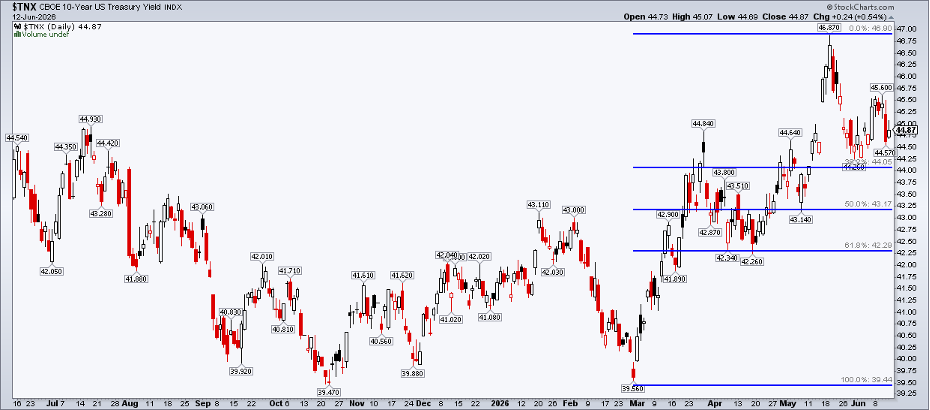

Oil Drops, Yields Follow

Today, following the news of a tentative framework peace deal between the U.S. and Iran, the benchmark 10-year Treasury rate ($TNX) flirts with a six-week low below 4.45%. If the truce holds and lower oil prices and interest rates play out, it may prompt the Fed to at least stay on hold (not raise rates).

Such a neutral stance would, in my view, be a net win for yield-sensitive plays like Real Estate and small-cap value.

Ahead of the policy announcement on Wednesday afternoon, let’s first take a closer look at the bond market, as the pieces could be fitting into place for a more dovish fixed-income backdrop.

One Inflation Gauge Cools

Starting with TIP:IEF (the iShares TIPS Bond ETF/the iShares 7-10 Year Treasury Bond ETF), we find that investors have gotten less worried about the inflation backdrop. This comes as dire headlines have printed one after another about soaring consumer prices. As often happens, the market was a few steps ahead of the economy. Technically, TIP:IEF failed at its April 2022 peak.

The onus is now on the bond vigilantes to hold support in the 1.164–1.1688 range on the ratio chart below. While the pair trades below its 50-day moving average, the long-term 200-day moving average is rising, suggesting it’s not an all-clear on the forward-looking inflation barometer.

What will it take for the Fed to consider cutting again? I think TIP:IEF would have to return to its pre-war low near 1.14.

Crude Oil: The Real Swing Vote

Turning to commodities, oil remains the X-factor for Chair Warsh, Governor Powell, and the rest of them.

WTI spiked above $119 at the YTD peak before printing a closing high of $112.95 on April 7. Having breached the April 17 settle of $83.85 this week, there’s a major air pocket down to the mid-$60s. Recall that WTI rallied in advance of the first strikes on Iran; it turned out that oil traders also sniffed out the bilateral agreement weeks ahead of time. Oil’s 200-day moving average will soon be near $75, and that could be the first battleground before the mid-$60s.

But what’s the old Wall Street adage? “Buy on the sound of cannons, sell on the sound of trumpets.” That would imply taking some profits on stocks and perhaps even buying the dip in oil. A gospel saying among technicians is, “Former support becomes new resistance,” which argues for the $84 to $87 zone being a new near-term ceiling for WTI. A small bounce to that range is possible this week, particularly with oil’s RSI plunging to its lowest level of the year.

A Possible Goldilocks Setup?

Before the Fed became a chatterbox and press conferences followed each meeting, macro strategists focused on three things: 1) growth, 2) inflation, and 3) guidance.

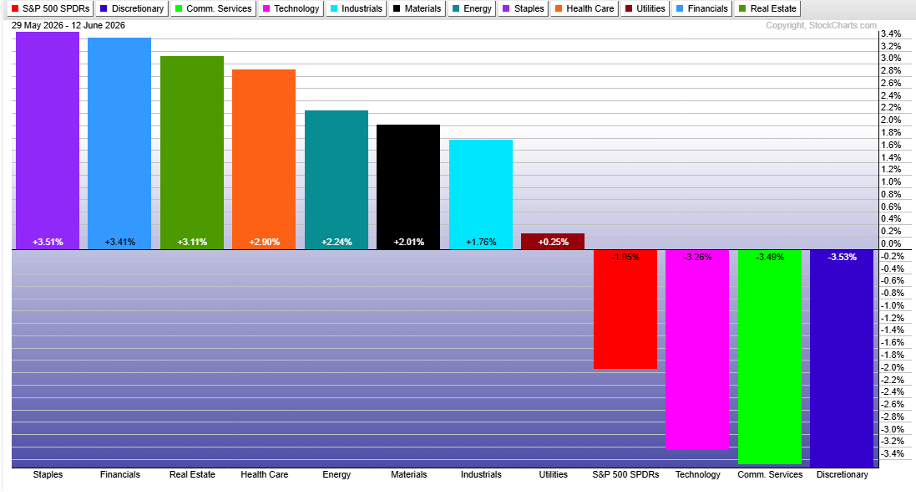

Market pricing of U.S. real GDP growth seems to be near 2%, though recent timely indicators point to a 3% real expansion pace. We can see green shoots of improved GDP sentiment in S&P 500 sector performance trends this month.

Indeed, since the beginning of June, Financials (XLF), Materials (XLB), and Industrials (XLI) have been among the leaders. Falling Treasury yields have been a boon to high-dividend-yield Consumer Staples (XLP) and Real Estate (XLRE), too. Amid the broadening, areas that tend to outperform amid economic-growth scarcity (Tech, Communication Services, and Consumer Discretionary, dominated by big TMT companies) have lagged.

Viewed through this lens and using some intermarket analysis principles, the stagflationary backdrop could morph into a Goldilocks environment of improved growth and in-check inflation. It’s not as far-fetched as it seems.

Are the Dot Plot’s Days Numbered Under the Warsh-Led Fed?

Those are the growth and inflation pieces that the centrists and doves on the Committee might home in on. As for its guidance, that’s anybody’s guess. This week’s meeting will feature the quarterly Summary of Economic Projections (the dot plot).

Warsh has not been a big fan of such forecasts, so focusing more on the Fed statement could be the better approach going forward (for those who are avid Fed watchers).

The Bottom Line

Ultimately, price action will be the first to know. Watch the 2-year and 10-year yields, TIP:IEF, and how cyclical industries perform. Geopolitics is difficult to predict, and counting on peace in the Middle East is a fool’s errand. For now, though, lower oil prices and lower rates appear to delay Kevin Warsh’s first big test as Fed chair.

Disclaimer: This blog is for educational purposes only and should not be construed as financial advice. The ideas and strategies should never be used without first assessing your own personal and financial situation, or without consulting a financial professional.